- Almost 100% of JPY trading is versus TONA at the moment.

- But all of this activity is in OTC derivatives.

- Euroyen TIBOR futures used to be a significant market before LIBOR cessation.

- TFX and JPX have just launched TONA futures, as a consultation for the permanent cessation of TIBOR is announced.

*I hope our readers don’t mind, but I chose to accept a little help from Bard this week. With so much web traffic generated via Google searches, I thought it a worthwhile experiment.

TIBOR Cessation

No two markets are the same, and we see this in the adoption of RFR trading. Whilst JPY LIBOR is but a distant memory, we still have JPY TIBOR as a legacy “non-RFR” rate in Japanese markets, somewhat competing with TONA. Early analysis suggested that JPY TIBOR “had a chance” but we recently saw a consultation published on the permanent cessation of Euroyen TIBOR:

Consultation responses are requested by 30th September 2023. We have mentioned many times, but it is striking how little data people use in their responses to consultations. Any opinions/subjective statements really need to be backed up by data, potentially making them objective. Please have a read of this blog and choose your data appropriately!

TONA Adoption

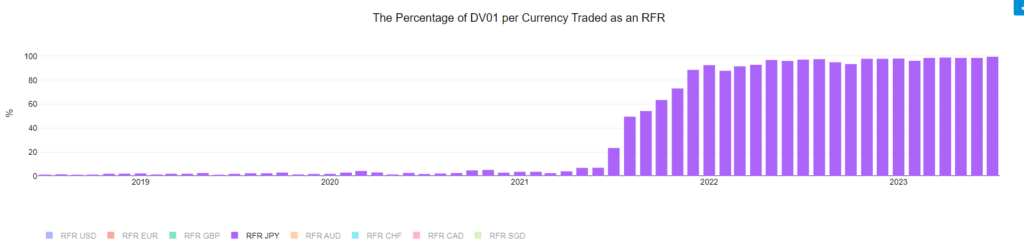

The ISDA Clarus RFR Adoption Indicator includes data on the adoption of trading in RFRs for 8 individual currencies. From rfr.clarusft.com:

Showing;

- The percentage of risk traded versus TONA in JPY interest rate derivatives (measured by DV01).

- This is across both OTC and Futures (ETD) markets.

- Non-RFR activity is defined as “Legacy rates” and include JPY LIBOR (pre-cessation) and TIBOR.

- Almost 100% of JPY derivatives are already trading versus TONA.

- So should we even care about TIBOR cessation?

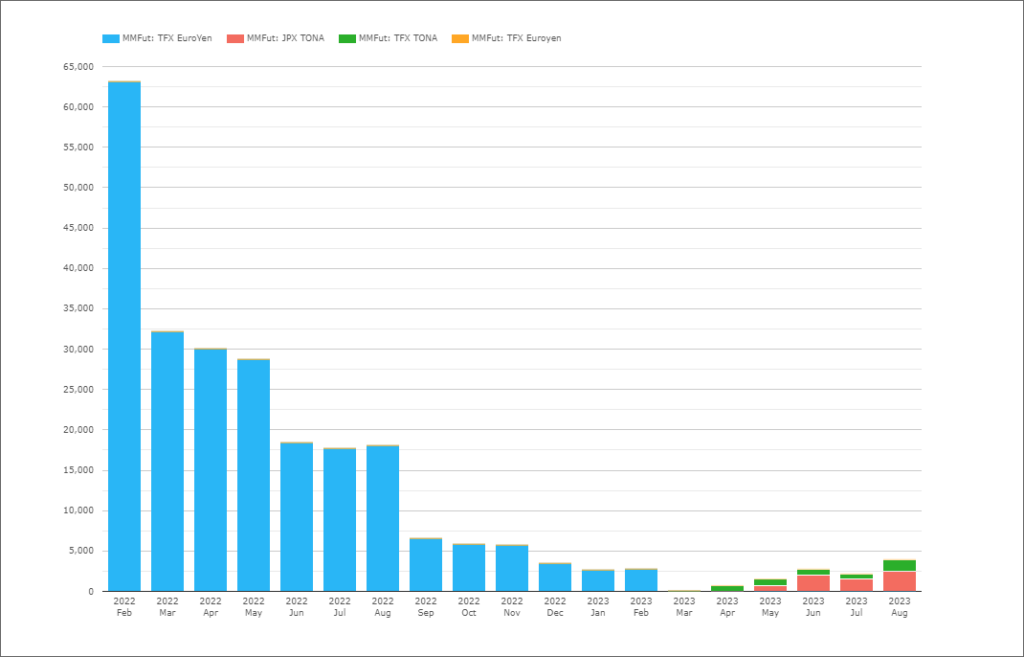

TIBOR Futures

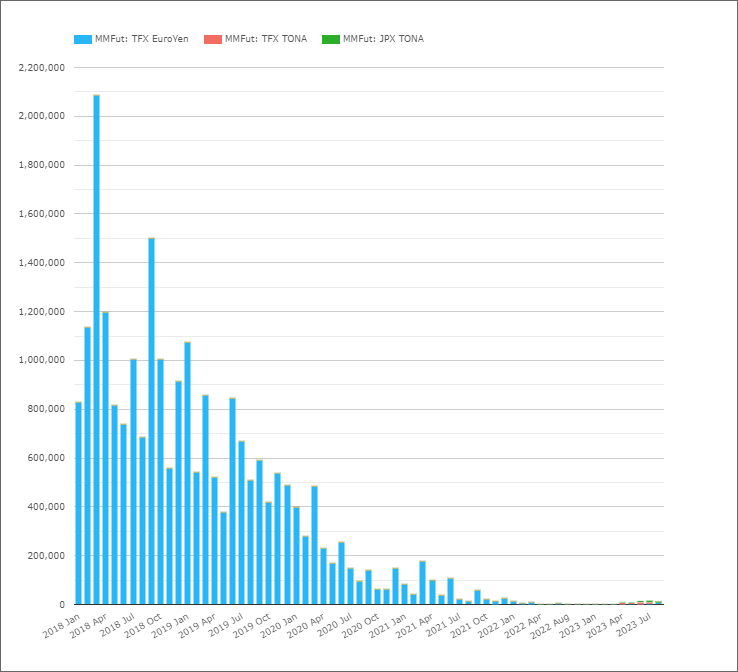

CCPView carries a decent history of trading volumes in JPY money market futures, and you can see that the market is a looooong way from where it once stood:

Showing;

- March 2018 saw over $2Trn equivalent traded in JPY short term interest rate futures.

- The past five years have seen volumes steadily decline (until very recently).

- The collapse in volumes suggests that swap-related hedging (mainly of fixing risk in JPY) was a big driver of risk appetite for TIBOR futures.

- Now, there are new products being launched.

So whilst the use of TIBOR in futures markets has already virtually stopped, there remains scope for a new bumper JPY futures product. This is undoubtedly why both TFX and JPX have recently launched new TONA contracts.

Competition

JPY TIBOR and LIBOR futures were always a bit tricky to decipher. At one point there were at least 4 exchanges listing a short term interest rate future in JPY. As we know from indices like SONIA, that situation is somewhat unusual, although to be fair the four products spanned both TIBOR and JPY LIBOR futures so were not identical.

In TONA futures, we have (so far) seen TFX and JPX throw their hats in the ring.

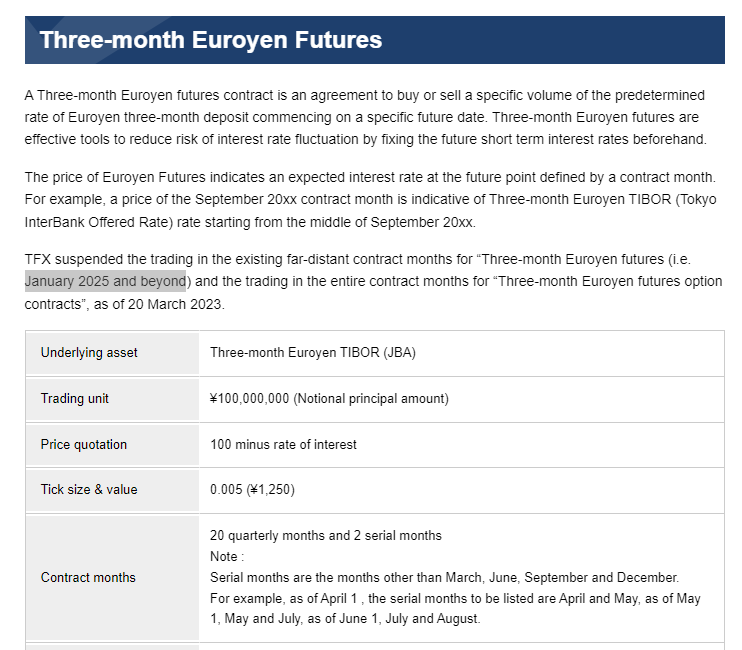

TFX TONA Futures

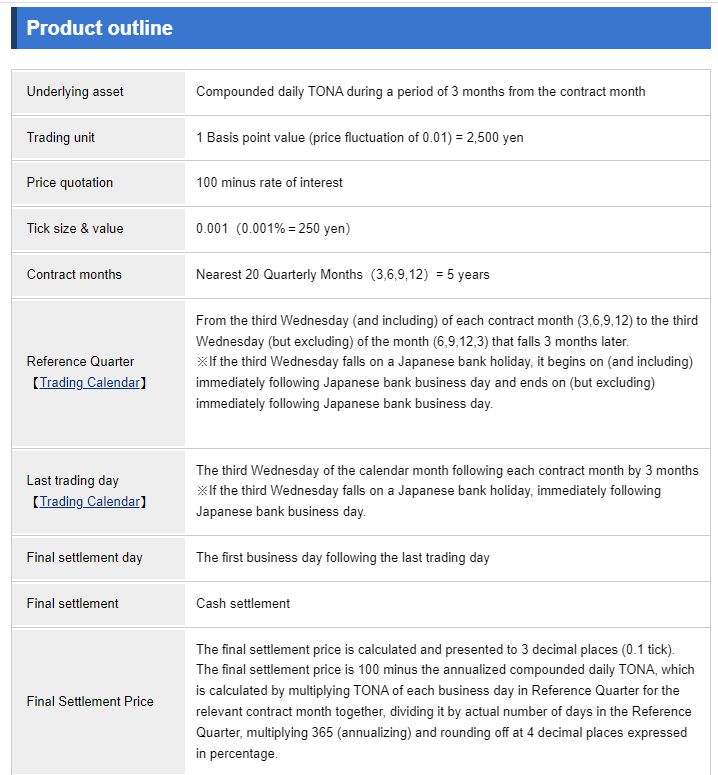

The TFX website is a great resource! I encourage our readers to head on over to their TONA page, where they include contract specs amongst other information:

In summary;

- IMM dated (still no BoJ-dated contracts then. Boo.).

- Three month maturity.

- JPY2,500 per basis point.

- Price defined as 100-interest rate.

- See our Mechanics and Definitions of Short Term Interest Rate Futures if any of these terms don’t make sense.

I couldn’t help clicking through to the Euroyen Futures page and I am glad I did! Trading in contracts maturing after January 2025 has now been suspended. Make out of that what you will in your consultation responses!

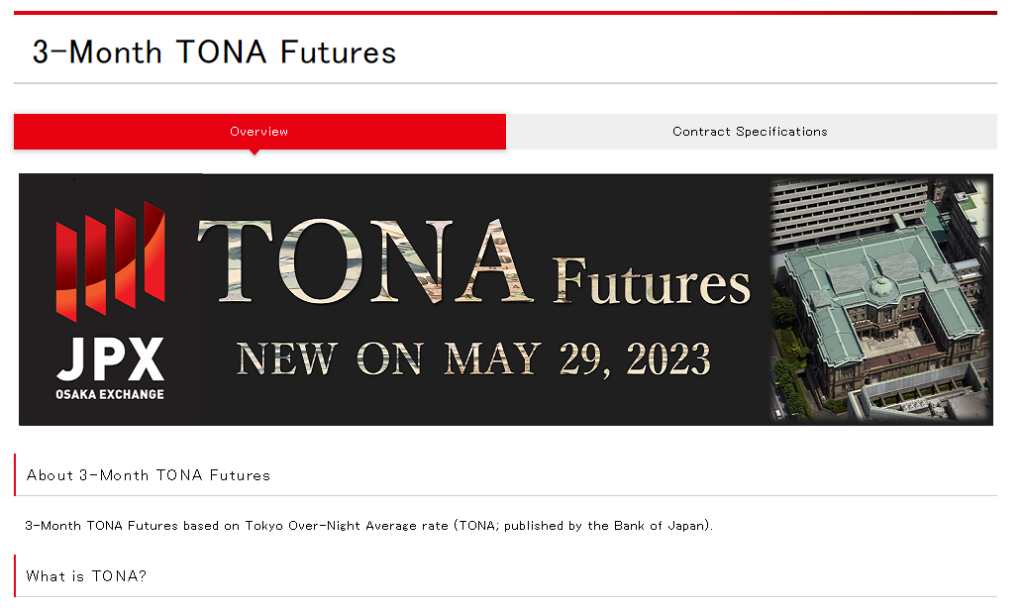

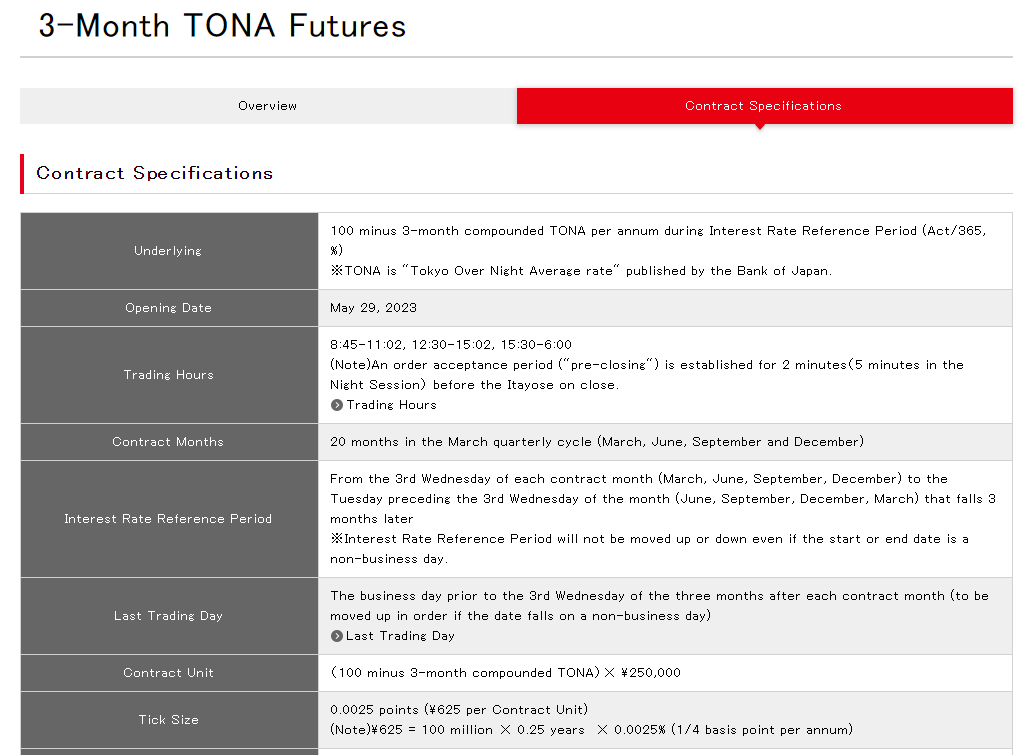

JPX TONA Futures

JPX threw their hats into the ring in May/June 2023:

The product outline with contract specs is again very clear:

In summary;

- IMM dated.

- Three month maturity.

- JPY2,500 per basis point.

- Price defined as 100-interest rate.

Yes, the TFX and the JPX contracts are identical! Both TFX and JPX have form in interest rate-related futures already. TFX offer the Euroyen TIBOR contracts, whilst JPX have the (very successful!) JGB contracts (in 5Y, 10Y and 20Y maturities).

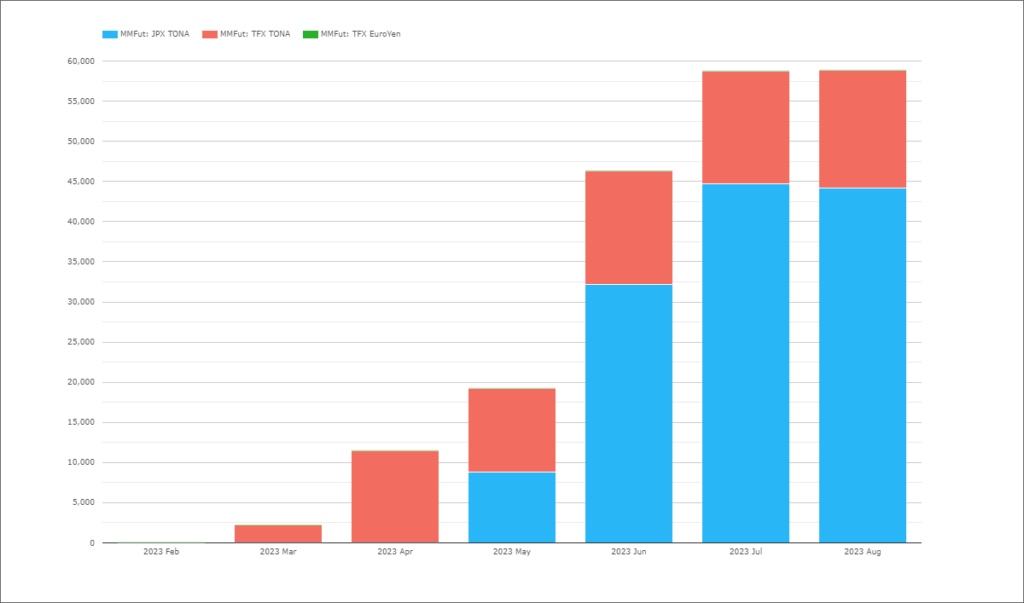

Volume Analysis

CCPView includes data on both the TFX and JPX TONA contracts since launch. It is very early days for the contracts:

Showing;

- We recorded zero volumes in February 2023 for JPY STIRs!

- The launch of the TONA contracts has changed that, with volumes reaching almost 60,000 contracts traded.

- August 2023 was a new record month for activity in TONA futures . Again, early days but the signs are good.

- Market share is split 75% at JPX plays 25% at TFX.

Open Interest

Finally, it appears that since the IMM roll in March 2023, the Euroyen TIBOR contracts now have zero Open Interest. And impressively, the Open Interest in the new TONA contracts already exceeds the Open Interest we saw in TIBOR contracts at the end of 2022:

I am sure that we will see continued growth in these TONA contracts as the market matures. Good news indeed for RFRs.

In Summary

- TFX and JPX have launched identical TONA futures.

- They are three-month, IMM-dated contracts.

- So far JPX have a 75% market share and TFX a 25% share.

- This comes as a consultation on the cessation of Euroyen TIBOR has been announced.

- We have already seen Open Interest in Euroyen TIBOR futures drop to zero.

Apologies if this is a “picky” comment, but wit would be awesome if you always include units on your Y-axis: even though you always give the reader a useful hint in the bullet points underneath each chart, I usually scan through the charts first and want to get a clear picture of what I am looking at: $ thousands notional? $ DV01? $ thousands DV01? Thank you 🙂 Otherwise another great blog post, thank you Chris.

Thanks for the comment Jan – you make a good point, well noted! (Post now updated)

Great article, Chris-san, but I would like to point out that something is wrong with the trading volume for TONA futures at TFX and JPX. According to both exchanges’ official stats, the monthly trading volume (contracts) and the trading shares must be as follows:

JPX TFX JPX share TFX share

Mar – 2,224 – –

Apr – 11,463 – –

May 8,834* 10,401 – –

June 32,221 14,111 70% 30%

July 44,716 13,996 76% 24%

Aug 44,130 14,656 75% 25%

*Launched on May 29th

Many thanks for pointing this out, and huge apologies to our readers for this original error. The post has now been updated to reflect the accurate data.