Q3 2025 rates swaps CCP competition

In our quarterly blogs on cleared rates swap volumes, we review CCP market shares across all currencies. However, only a few currencies show meaningful competition between clearinghouses. This blog focuses on the competitive dynamic in those competitive currencies. Key takeaways: In Q3 2025, only four currencies – EUR, JPY, CNY, and INR had more than […]

Volumes and most active names in credit derivatives – September 2025

Today we look at issuer names most actively traded based on CDS trades reported to US SEC Securities Based Swap Data Repositories (SBSDRs) in September 2025. Background The prior similar blog covered credit derivatives (CRD) for July 2025. Given the CDS-market peaks naturally in March and September, we will focus on those months going forward. […]

Swaption volumes by strike – Q3 2025

This post looks at USD swaptions activity in Q3 as part of our regular quarterly coverage, the most recent of which was Swaption Volumes by Strike – Q2 2024. We use SDRView data, which shows all trades reported by US financial firms to US SDRs. If you are new to swaptions, some basics are outlined […]

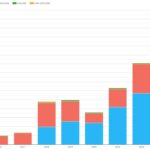

Derivatives innovation: SOFR futures, TONA futures, MYR swaps

Today, we look at three recent start-ups or new products introduced by derivatives exchanges and clearinghouses (CCPs). Key takeaways: All the charts, data, and statistics in this blog were sourced from CCPView. FMX rates futures FMX is a fixed income e-trading platform focused on US Treasury bonds, FX, and repo owned by BGC. Recently, FMX launched the […]

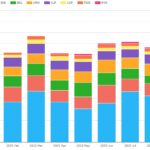

CRD volumes at the end of Q3 2025

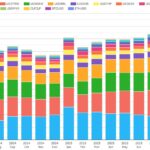

This blog covers the volumes, of credit derivatives (CRD) in September 2025, as submitted to us by CCPs, and as reported to US SDRs and SBSDRs. Key takeaways: A year-on-year (YoY) comparison of notional volumes between September 2025 and September 2024 shows that: All the charts, data, and statistics in this blog were sourced from CCPView and SDRView. Cleared CRD volumes First, we look at cleared CRD by currency. Chart 1: All CRD […]

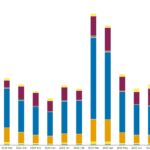

FX derivatives volumes at the end of Q3 2025

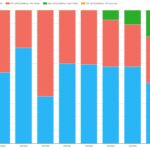

This blog covers the volumes of FX derivatives (FXD) in September 2025, as reported by CCPs and to US SDRs. Key takeaways: A year-on-year (YoY) comparison of volumes between September 2025 and September 2024 shows that: Analysis by product group showed that clearing rates for NDFs on deliverable pairs are aligned with those for FX […]

Reset optimization: part 2 – SPS activity

In part 1 of this blog, we promised to follow up with part 2. Here it is. Key takeaways Background In Part 1, we estimated that, of the $31.1 trillion SDR-reported FRA activity in H1 2025, reset optimization-driven FRA spike days from OSTTRA’s Reset service and Tullett Prebon’s Matchbook service (formerly “tpMatch”) totaled $25.0 trillion. […]

What’s new in CCP Disclosures – Q2 2025?

Clearing houses have published their latest CPMI-IOSCO Quantitative Disclosures for Q2 2025. Key takeaways Background Under the CPMI-IOSCO Public Quantitative Disclosures, central counterparties (CCPs) publish over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing, and more. CCPView has more than 8 years of these quarterly disclosures for 44 clearinghouses, each with multiple Clearing […]

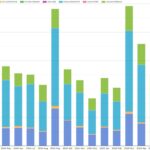

What’s new in JPY swaps in 2025?

Following our blog in April 2024, we further explore the volume expansions and market transitions in JPY IR derivatives. Key takeaways Cleared OTC interest rate derivatives (IRD) volumes As noted in our quarterly CCP IRD volumes blog, JPY IRD volumes exploded in 2024 and 2025. I wanted to look over a longer period to see […]

Volumes and most active names in credit derivatives – July 2025

Today we look at issuer names most actively traded in trades reported to US SEC Securities Based Swap Data Repositories (SBSDRs) in July 2025. The prior similar blog covered April 2025. Today’s iteration also includes a brief review of overall single-name CDS volumes. CDS on sovereigns We start with USD CDS on sovereign names. Table […]