Is volatility in RFR Adoption here to stay?

Volatility in Rates markets has been elevated this year. However, I cannot remember a year when we haven’t said similar by October! It is very likely that the human-bias is innately more sensitive to change than stasis, which then leads inquisitive minds to work out what is causing the change. But one thing that is […]

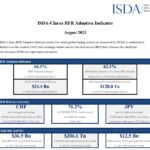

RFR Trading Is Now Back on Track – August 2023

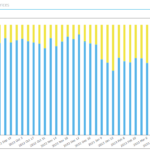

The ISDA-Clarus RFR Adoption Indicator for August 2023 has now been published. Showing; Highlights Can the narrative cloud the facts? I feel like that is the case with RFR Trading. Look at headline adoption of RFRs in 2023: Plus; This is against a backdrop on the Clarus blog, whereby we have noted: The August 2023 ISDA-Clarus […]

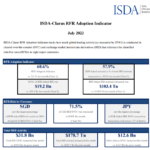

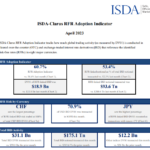

RFR Adoption July 2023

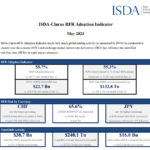

RFR Adoption is Increasing Again The latest edition of the ISDA-Clarus RFR Adoption Indicator was published earlier this week. You can find the full report over on the ISDA website here. As always, we provide a look into the data: Showing; SOFR Trading Increases As long-time readers well know by now, USD markets (and hence […]

We Need to Talk About the Clarus API

Most of our readers come to the Clarus blog to receive new information from us. Whether that be on the data side (such as the monthly RFR Adoption Indicator) or about new regulations (such as Central Clearing of Bonds and Repos). But do our readers ever stop to consider which tools we use to deliver […]

Bollinger, Greenspan and The Millennium Bug: LIBOR Is Now Dead

USD LIBOR is no more: I will likely never type US0003M into my Bloomberg ever again. I doubt many will shed a tear at the ultimate demise of LIBOR because: LIBOR – The Numbers This is as good a time as any to therefore pause and consider some of the things we saw in USD […]

The Latest on Canada and the Transition from CDOR to CORRA

ISDA recently published a very informative webinar on the CDOR Transition: From this, I learned that 30th June 2023 (i.e. Friday!) is a big day for Canada Rates markets. Succinctly, no more new CDOR trading should take place after this date, other than for some well-defined exceptions. The CARR website is a great resource (from […]

Find Out What Was Weird About RFR Trading In May

The latest ISDA-Clarus RFR Adoption Indicator has been published for May 2023 so I asked ChatGPT about the next report: I love how it states that because it is a language model it doesn’t predict the future. Rather than simply stating “you cannot predict the future smart @rse”. From my experience with ChatGPT, I found […]

Now LCH Have Converted Your USD Swaps too!

As recently as January I posed the question: That blog was written in response to the fact that 2022 continued to see plenty of USD LIBOR risk sent to CCPs. Could all of that trading just stop in time for the final cessation of USD LIBOR in June 2023? Following on from the recent CME […]

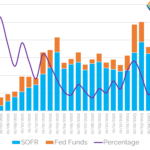

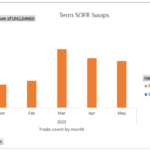

Term SOFR and BSBY Swap Volumes – May 2023

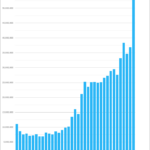

I last looked at Average and Term SOFR Volumes and Term SOFR and BSBY Volumes in early February 2023, focusing on 2022 volumes, so today I wanted to look at the 2023 data trends for these reference indices. As before we will seperate Term SOFR (published by CME) from Average SOFR (NY Fed), see the […]

Do you know how much now trades in RFRs after the CME conversion exercises?

We’ve covered the CME conversion exercises in detail here on the Clarus blog because they were really significant events for market participants and for the broader transition to SOFR in US markets. You can catch up on the recent publications below: All of these blogs were written before we could assess the overall impact to […]