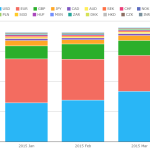

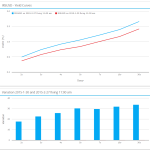

March 2015 Review – Bloomberg out in front

Bloomberg are #1 for SEF liquidity in Q1 2015 whilst Tradeweb saw the highest overall volumes. We saw record USD Swap volumes reported to the SDRs in March 2015, with our review highlighting increasing compression activity. The great month for the industry was rounded-out with over 60% of volumes traded across a SEF. USD IRS On-SEF $1.56trn in notional traded across SEFs during March […]

SDR Alerts, Terminations and Screen Real Estate

One of the challenges we face in a world of mass information is getting our applications to be always open and used on a desktop or mobile device. Even in the Capital Markets domain with six or nine monitors common on a traders desk, it is not easy to achieve this. So much news, information, data […]

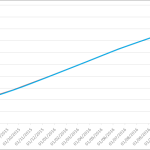

The IMM Roll for Swaps – What is it and what are the volumes?

Every quarter, monthly SEF volumes are distorted artificially higher by IMM roll activity. What is it and how can we identify the trades? The History of the IMM Roll The International Monetary Market (IMM) was a division of the CME back in the 1970s. There is a great essay here for the history buffs. In […]

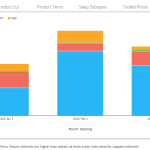

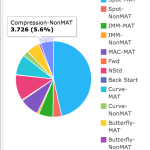

Compression List Trading On SEFs

Compression List Trading volumes have continued on their upward trend this year and in this article I will look into the what the data shows both in terms of volumes and also SEF market share. On SEF Compression Lists By Month Lets start with an SDRView Res chart of monthly gross notionals in G4 currencies […]

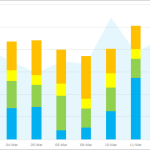

Spreadovers: US Treasury Spreads in the Swaps Data

US Treasury Swap Spreads (“Spreadovers”) are a significant portion of the Swaps market. Up to 1 in 5 trades are identified as a Spreadover, which helps us understand the SDR trade universe in even more detail. As a result, the curated Clarus data now augments over half of all trades from SDRs to enable greater transparency. We continue to refine our […]

Trade Surveillance in Swaps Trading

Swap Execution Facilities (SEFs) and Swap Data Repositories (SDRs) mean that it is now possible to implement effective Trade Surveillance in the OTC Swaps market and to do so in an analogous manner to the Futures market. Swap Dealers or Major Swap Participants can and should compare their executed trades with the trades reported in […]

Come on, feel the noise!

Better than an Oasis b-side, we thought what better time to talk about volatility than just after a payrolls report that saw 10 years move by over 12bp? Will the Fed in action be good for the SEF industry? I think we all know the supposition here. Volatility leads to increased trading, increased trading leads to higher […]

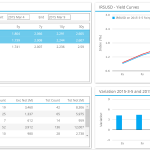

February 2015 Review – ICAP vs Bloomberg

Bloomberg and ICAP are fighting it out for the number one position in our latest monthly review of Interest Rate Swap volumes. We show that February looked a lot like January for both SEFs and CCPs, and that nearly 25% of risk was traded as part of a strategy. USD IRS On-SEF Broadly speaking, February 2015 looked a lot like […]

Our Response to the ESMA Consultation

We recently responded to the European Securities and Markets Authority (ESMA) Consultation Paper on a “Review of the technical standards on reporting under Article 9 of EMIR”. This consultation is on the revision of the Regulatory Technical Standards (RTS) and Implementing Technical Standards (ITS) of EMIR which deal with the obligation of Counterparties and CCPs […]

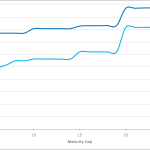

Swap Curve and Fly Trading: What goes in, must come out

Curve and Fly trading looks like a simple old game – existing trades are ripped-up and replaced with spot-starting hedges. So why don’t people do that across the Bloomberg SEF? Curve and Fly Trades Today, we indulge in a little bit of data mining for our recently launched Curve and Fly feature. This is a fascinating […]