Spreadovers: US Treasury Spreads in the Swaps Data

US Treasury Swap Spreads (“Spreadovers”) are a significant portion of the Swaps market. Up to 1 in 5 trades are identified as a Spreadover, which helps us understand the SDR trade universe in even more detail. As a result, the curated Clarus data now augments over half of all trades from SDRs to enable greater transparency. We continue to refine our […]

Trade Surveillance in Swaps Trading

Swap Execution Facilities (SEFs) and Swap Data Repositories (SDRs) mean that it is now possible to implement effective Trade Surveillance in the OTC Swaps market and to do so in an analogous manner to the Futures market. Swap Dealers or Major Swap Participants can and should compare their executed trades with the trades reported in […]

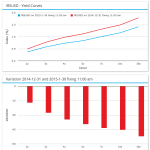

Come on, feel the noise!

Better than an Oasis b-side, we thought what better time to talk about volatility than just after a payrolls report that saw 10 years move by over 12bp? Will the Fed in action be good for the SEF industry? I think we all know the supposition here. Volatility leads to increased trading, increased trading leads to higher […]

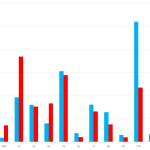

February 2015 Review – ICAP vs Bloomberg

Bloomberg and ICAP are fighting it out for the number one position in our latest monthly review of Interest Rate Swap volumes. We show that February looked a lot like January for both SEFs and CCPs, and that nearly 25% of risk was traded as part of a strategy. USD IRS On-SEF Broadly speaking, February 2015 looked a lot like […]

Our Response to the ESMA Consultation

We recently responded to the European Securities and Markets Authority (ESMA) Consultation Paper on a “Review of the technical standards on reporting under Article 9 of EMIR”. This consultation is on the revision of the Regulatory Technical Standards (RTS) and Implementing Technical Standards (ITS) of EMIR which deal with the obligation of Counterparties and CCPs […]

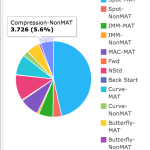

Swap Curve and Fly Trading: What goes in, must come out

Curve and Fly trading looks like a simple old game – existing trades are ripped-up and replaced with spot-starting hedges. So why don’t people do that across the Bloomberg SEF? Curve and Fly Trades Today, we indulge in a little bit of data mining for our recently launched Curve and Fly feature. This is a fascinating […]

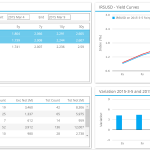

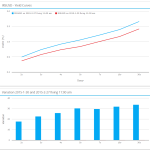

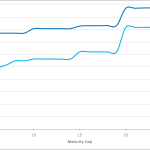

Inflation Swaps: What the Data Shows

As LCH SwapClear plans to start clearing Inflation Swaps I thought I would look at what the US SDR data shows for this product. While this is only part of the global market, it still provides very interesting insight into the market. Summary Inflation Swaps trade in USD, EUR, GBP Gross Notional volume averages $2 billion […]

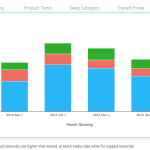

Swap Curve and Fly Trades: A quarter of all trades are not what they first seem

We now identify package trades within SDR data in real-time. These packages represent 25% of reported trades. Users can access this analysis via our SDRView Pro application, further increasing the utility and transparency of the data within OTC markets. This is a good example of how we can add simplicity and clarity to the data […]

ECB QE and EMIR Reporting. More transparency please!

Will ECB QE affect European Cross Currency swap markets? We need more transparency in European OTC data to definitively answer that question. In this blog, we use 2014 data from the SDRs to first examine what has traded over the past twelve months and then we take a quick look at 2015 data and discover a […]

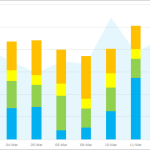

January Volumes in Swaps, Compression To the Fore

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in January 2015. First the highlights: Decent volumes but lower than December. Surprising given the large price moves, with 30Y down 50bps and 9 out of 22 days with >5bps moves in the 5Y. Global USD IRS volumes show LCH SwapClear with […]