- SACCR is the Standardised Approach to Counterparty Credit Risk (CRE52 under the consolidated Basel capital framework).

- It covers calculations for Credit Risk Weighted Assets and exposures under the Leverage Ratio (known as the Supplemental Leverage Ratio, SLR, in the US).

- It will impact the amount of Tier 1 capital banks must hold.

- SACCR means that Leverage Ratio calculations are now based on net risk, not on gross notional.

- SACCR will impact even those firms using the IMM (internal model method) for credit exposures because SACCR not only impacts the leverage ratio but also introduces floors to the outputs of IMM calculations.

- It is a standardised model that is designed to be more risk sensitive than its predecessor, the Current Exposure Methodology.

- Exposure at Default for a given counterparty is the core output of the SACCR model.

Five Years in the Making

We first started writing about SA-CCR – The Standardised Approach to Counterparty Credit Risk – in 2016! Over 5 years later, and banks are finally “turning on” SACCR.

Our expectation is that SACCR will fundamentally change bank behaviour over the coming years as SACCR-specific metrics are targeted by resource optimisation groups at dealer banks (XVA, resource management, regulatory capital).

What is SACCR?

The acronym is a little misleading in my opinion. What does the Standardised Approach to Counterparty Credit Risk actually do?

- It introduces a risk-based measure of exposures. It largely replaces the Current Exposure Methodology in the Basel capital framework for banks.

- It is used to calculate the exposure for banks of “off-balance sheet” derivatives. Any derivative in FX, Rates, Equities, Commodities etc. will be captured by SACCR.

- From a conceptual viewpoint, by making measures more risk-based, SACCR should be a “fairer” representation of the actual risks being run by banks. Of course, any standardised model has its limitations, but replacing a gross-notional based measure such as the Current Exposure Methodology with a net-risk based measure is expected to result in a more accurate representation of risk.

What is SACCR Used For?

SACCR impacts the capital requirements of any given bank in a number of ways:

- Credit Risk Weighted Assets. For most banks (i.e. excluding the huge broker-dealer/global banks who tend to dominate the industry!), the immediate impact of SACCR is to change how Credit exposures are calculated versus any given counterparty. The total Risk Weighted Assets for a Credit exposure will now be calculated by:

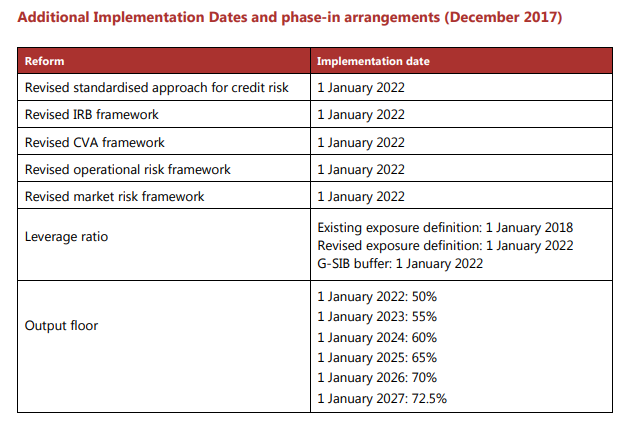

Credit RWA = EAD under SACCR x Counterparty Risk Weighting - Capital Floors. Many large banks (both global and large regional banks) have successfully applied for and been granted approval to use the “Internal Model Method” for calculating credit exposures across their franchises (so called “IMM” banks). These internal models will have many benefits – such as offsetting credit exposures generated across different asset classes for a given counterparty – but they tend to be a “black box”. We can imagine they are all somewhat similar and act much like an Initial Margin model (and probably using a parametric calibration so that they don’t move around too much). However, SACCR will still impact IMM banks. This is because the Basel capital regs are (slowly) introducing capital floors (already live in the US with the “Collins Floor”), which are calibrated to SACCR. The table below best summarises the impact of the floors:

- The timelines have likely changed since the table above was published over 4 years ago, but you get the idea – even banks using internal models to calculate credit RWAs will be impacted by SACCR. If their models output a credit exposure that is less than 50% as calculated under SACCR, then the SACCR calculated value will “kick in” and the standard SACCR model will effectively be used to measure Credit RWAs.

- Leverage Ratio: This is potentially the “big one” for SACCR. When the leverage ratio was introduced, in response to the GFC, it was intentionally done so in a crude manner, in efforts to throttle back extensive use of off-balance sheet exposures. Prior to the GFC, these exposures, largely derivatives, did not generate sufficient regulatory capital buffers to protect banks (and their investors) in the event of severe market stresses. The Leverage Ratio continues to be a key pillar of post GFC financial reforms, along with clearing mandates and uncleared margin rules. Any changes to it are therefore BIG NEWS. If you take one thing away from this blog, SACCR means that the leverage ratio is now based on net risk, not on gross notional.

- Bank Capital. Tying in all of our previous points here, a bank will typically have one of two constraints – either Leverage Ratio or Credit RWAs. This is because a bank has to hold a given pot of capital versus its exposures, and these exposures are not necessarily additive. It simply has to hold enough tier one capital (typically equity, with some convertible debt) to satisfy the highest of the two requirements. For example, a bank may hold 7.5% Tier 1 capital versus it’s exposures as calculated under the leverage ratio, and 15% Tier 1 capital versus its total Risk Weighted Assets (of which Credit RWAs are one component). They do not then hold a total of 22.5% Tier 1 capital versus their exposures. The same Tier 1 capital is counted in each ratio – essentially the numerator is the same, the denominator changes.

Components of SACCR

There are certain key components and concepts to be aware of under the SACCR calculations. As we have covered previously, the overall calculation for exposures under SACCR can be summarised as:

EAD = Alpha * (Replacement Cost + Multiplier * AddOn)

What do these mean?

EAD and PFEs

Under the Current Exposure Methodology, we were always obsessed with PFEs – Potential Future Exposures. These were broadly calculated on a gross basis (i.e. a short vs a long position with the same counterparty was counted as “double long” if held as two trades) and the PFE’s were calculated according to maturity, gross notional and asset class. The BIS table below summarises it well – as well it should, this table has been around for over 30 years!

A little confusingly, PFEs are indeed still calculated as part of the SACCR methodology, but they are calculated in a different manner, and sum up into the “AddOn” component above. Generally, we tend to speak about Exposure at Default (EAD) under SACCR and Potential Future Exposures (PFEs) under CEM. For the less geeky, we can just consider them “exposures” under each methodology.

Key Terms

To understand the driving factors under SACCR, we need to consider the following:

- Alpha. This is a regulatory defined term of 1.4. What does this mean? It inflates all of the calculations under SACCR by 40%, therefore any non-zero element of a SACCR calculation effectively attracts a 40% “add-on” that was not there under CEM.

- Replacement Cost. This can be broadly considered the mark-to-market of a derivatives position, net of any collateral held against it. That collateral may attract certain haircuts, and may even not relate to the mark to market today (due to delays in settlement, there is typically a one-day lag between collateral being calculated and it settling). RC is therefore very rarely zero and can introduce real noise into SACCR calculations.

- Multiplier. This is a very interesting term and is very sensitive for unmargined portfolios. It is designed to reflect the fact that a deeply in the money position is unlikely to quickly flip to in the money (and vice versa). It can also help reflect the fact that over-collateralised positions carry less risk than under-collateralised ones.

- Add on. This is a bit of a “catch-all”, simply referring to the underlying calculations that we perform at a trade level to define the actual exposures generated by numerous different types of derivatives. This “Add-On” is the main target of our Clarus SACCR Calculators. The Add-On depends on the following:

- Asset Class – Rates, FX, Credit, Equities, Commodities.

- Hedging Set – what is the primary risk factor of a derivative? For FX instruments, this is the currency pair (EURUSD forms a different hedging set to GBPUSD). For Rates, it is defined by time to maturity AND currency, but ignores index.

- Adjusted Notional – for linear FX, this is simply the net sum of all of the positions within a currency pair. FX Options offset FX Forwards, currency swaps are even included. There is a single netting bucket per currency pair, that has a single “Adjusted Notional” related to it. Options have a simple Black-Scholes delta calculated, according to strike, underlying and time to expiry. Rates have a “delta” calculated per maturity and these are summed within each maturity bucket and then certain offsets are allowed across maturity buckets.

- Maturity Factor. The really novel part of SACCR is the Maturity Factor. This is dictated by the margin agreement (or lack of one) that governs the counterparty relationship. Different margin agreements (CSAs) will carry different “Margin Periods of Risk”, that will change the maturity factor applied to the Adjusted Notional of the overall counterparty relationship. For unmargined netting sets, the calculation of the Maturity Factor is sensitive to either the overall maturity of the trade or when it next “resets” or settles to market.

Part Two

This is only the start of the story for SACCR. I’ve provided some critical background here to the terms and concepts. Next up, Part Two of our Mechanics and Definitions of SACCR will cover more about the maturity factor and how different CSAs and treatments of derivatives impact the EAD calculations.

In Summary

In this Part One of our Mechanics and Definitions of SACCR series, we look at;

- SACCR as a risk-based measure of counterparty exposure, replacing the gross notional based Current Exposure Methodology.

- How SACCR impacts not only Credit Risk Weighted Assets, but also Leverage Ratio calculations.

- The output of SACCR as Exposure at Default, a function of net notional exposures and margin agreement (CSA)-specific metrics.

- How the regulatory multiplier, alpha, at 140% impacts all non-zero inputs to the SACCR calculations.

- Where netting applies under the model.

Next up, we will examine both the maturity factor and the multiplier that play such pivotal roles in the SACCR calculations.