Following on from the surprise entry of our NOK Rates blog in the Top 10 Clarus blogs of 2019, it is high time I updated it with both a look at whether OIS is trading yet and what has happened in the world of NOWA since we last wrote about it in April 2019. And it gives me a chance to use some puns to brighten your January.

Scandie OIS Trading

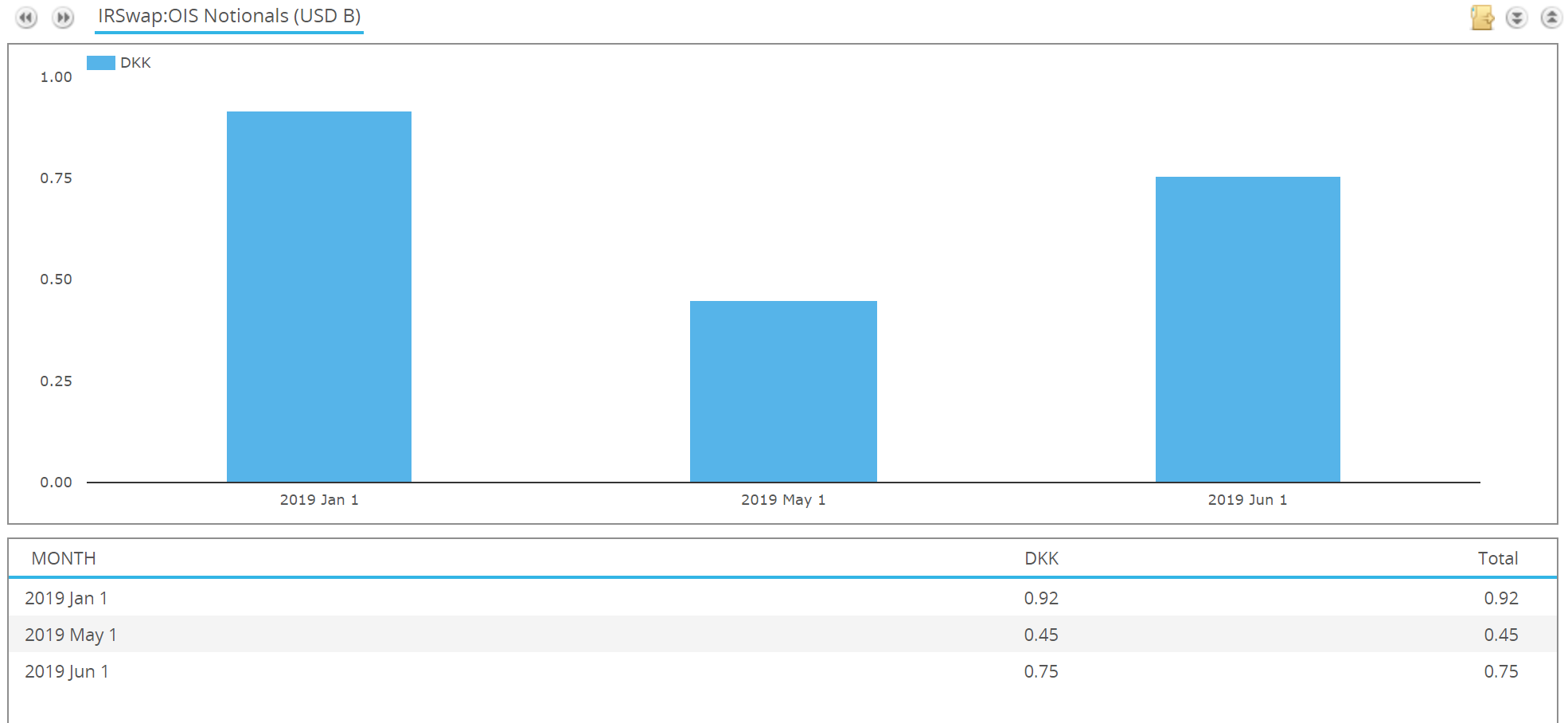

Looking at the LCH website shows that OIS is still not cleared in SEK, NOK or DKK:

Before the financial crisis, the order of market developments used to be:

- Create new product.

- Trade new product bilaterally.

- Develop liquidity in inter-dealer market.

- Finally think about clearing the thing once it gets too big and/or causes problems.

Nowadays, with the introduction of SOFR and €STR clearing having preceded the development of bilateral liquidity, that order seems to have been flipped on its head.

Maybe markets are looking to the CCPs to launch Scandie OIS clearing before any liquidity develops?

What this means is that there were no SEK OIS (STINA) nor NOK OIS (NOWA) reported to US SDRs in 2019. There were less than five DKK CITA trades all year:

The Time is NOWA?

A lot of work has been done, seemingly on the back of EURIBOR reform, to make SEK STIBOR, NOK NIBOR and DKK CIBOR compliant with the Benchmark Regulations in Europe. Some of these unsecured lending rates have interesting features that might make them pretty robust, such as the “entitlement element” of SEK STIBOR.

However, there is nothing like having a true Risk Free Rate to actually trade.

Therefore, please step forward NOK NOWA, 2020 version:

From the 1st January 2020, NOWA is now administered by the Norges Bank.

A Loro Loro Accounts

The original proposal from the Working Group in Norway suggested an Expanded NOWA would be used, as covered in our original NOK NOWA Rates blog.

However, at the August and September meetings last year, Norges Bank put forward a Reformed NOWA instead. This has a new definition and a new contingency method. Reading through the minutes of the Working Group, the crux of the argument seems to be:

Expanded Nowa [is] based on a large portion of foreign banks’ deposits [which] is problematic. It was pointed out that foreign banks’ deposits cannot be traded in an active market and the pricing of these deposits has little information value

Working group for alternative reference rates in NOK Meeting minutes, August 2019

This argument was expanded upon in the final proposal from the working group in September 2019. In the report, the concept of “Loro deposits” was introduced, which is something completely new to me.

Originating from foreign banks, it seems that Loro deposits are placed on unrepresentative rates of interest and are particularly punitive from a Liquidity Coverage Ratio perspective (LCR).

The irony that banks suffer from having a-loro deposits in this day and age shouldn’t be lost on anyone reading this blog (that pun is one for our resident Scouser at Clarus).

In summary;

A reformed Nowa also seems to be more robust to manipulation than an expanded Nowa. An expanded Nowa is affected by the interest rates foreign banks receive on their loro accounts in Norwegian banks. And even if there is no direct manipulation, the reference rate could be sensitive to changes in the rates on loro accounts. A reformed Nowa, which primarily reflects trades in central bank reserves between banks with an account at Norges Bank, seems more robust in the light of this criterion.

Report with a Recommendation for an Alternative Reference Rate in NOK, September 2019

NOWA ‘pinion

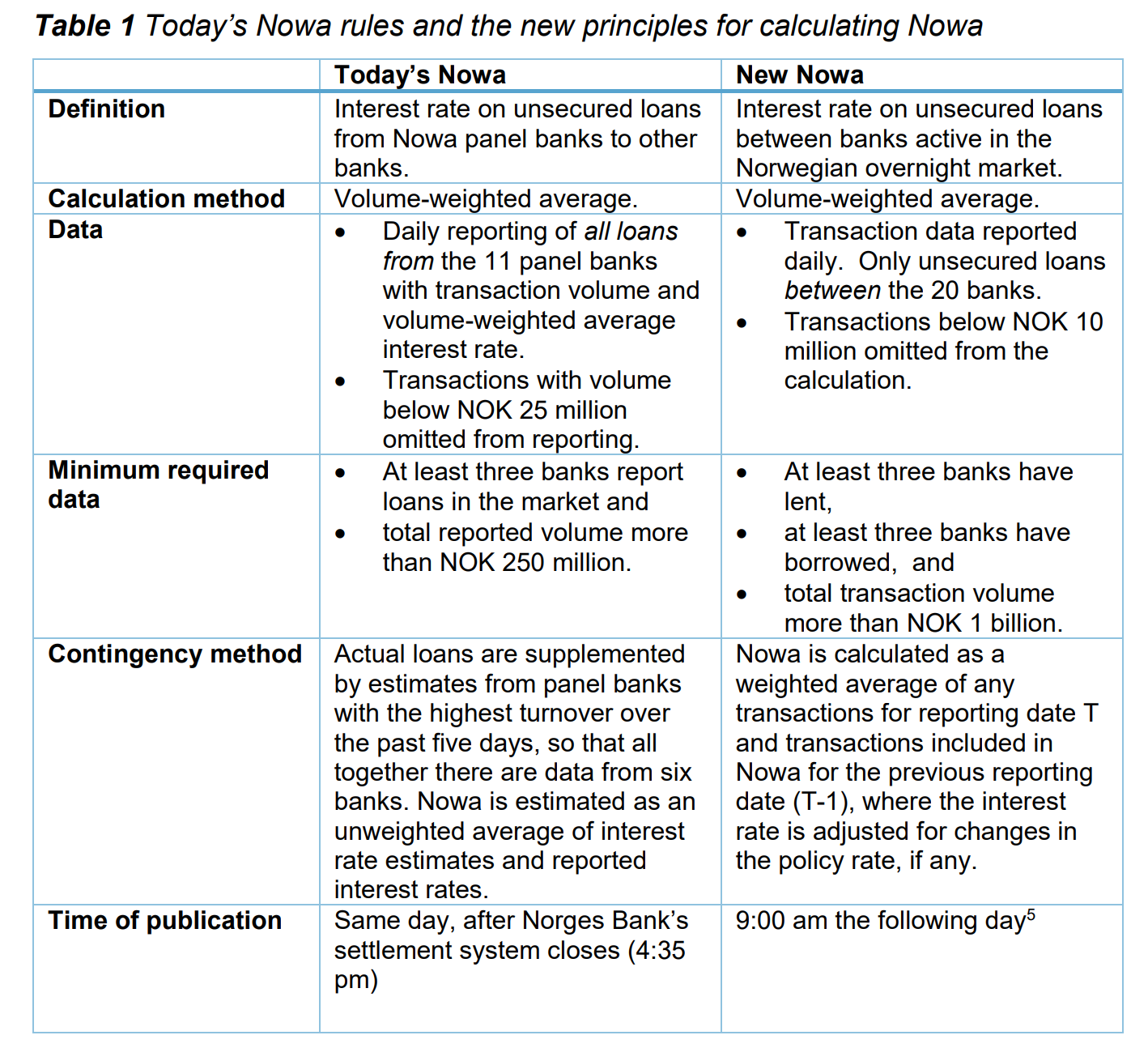

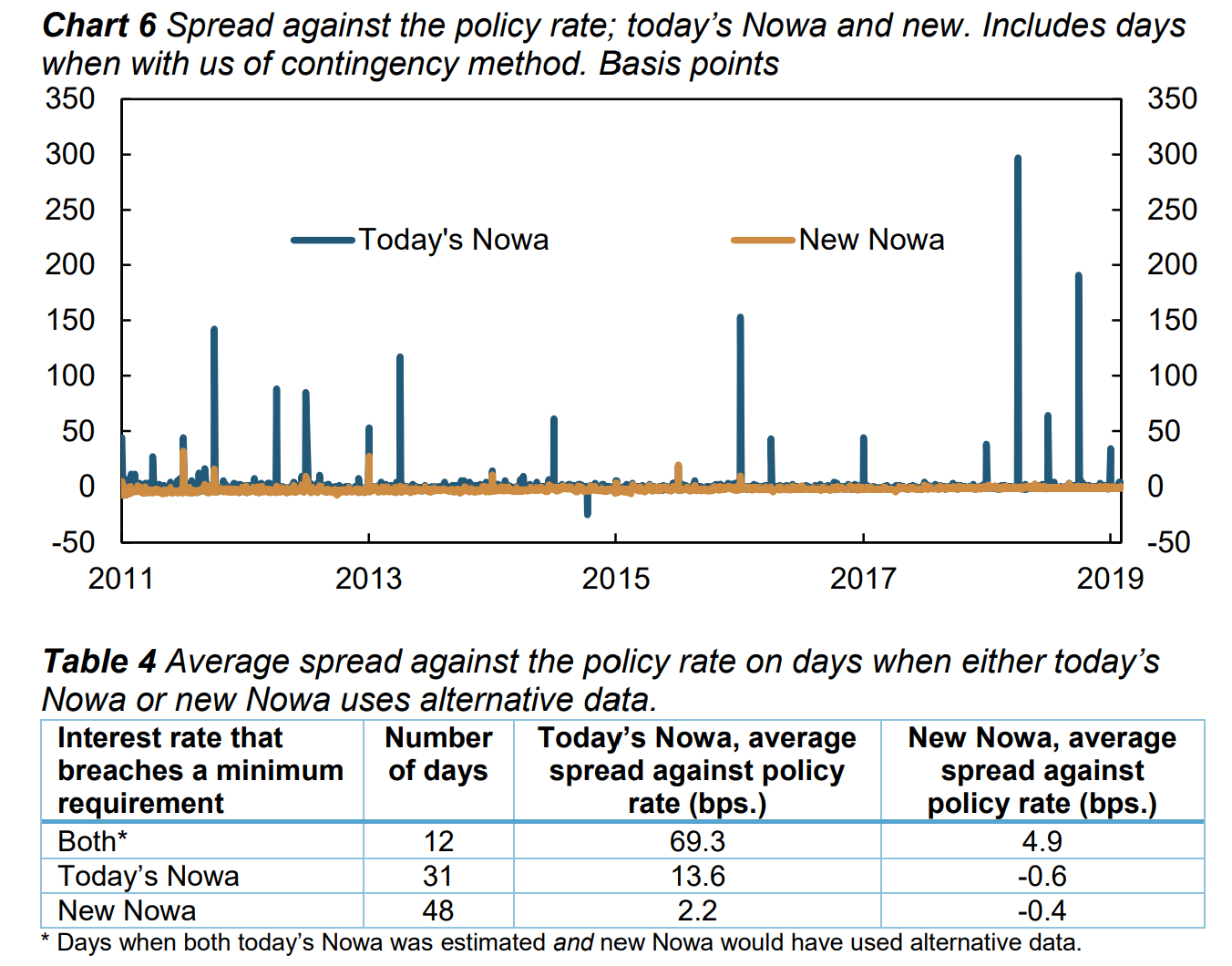

Therefore Expanded NOWA was dropped in preference of a “2020” version of NOWA. This Norges Bank paper highlights the resulting differences between old NOWA (confusingly called “today’s” NOWA in the table) and 2020 NOWA:

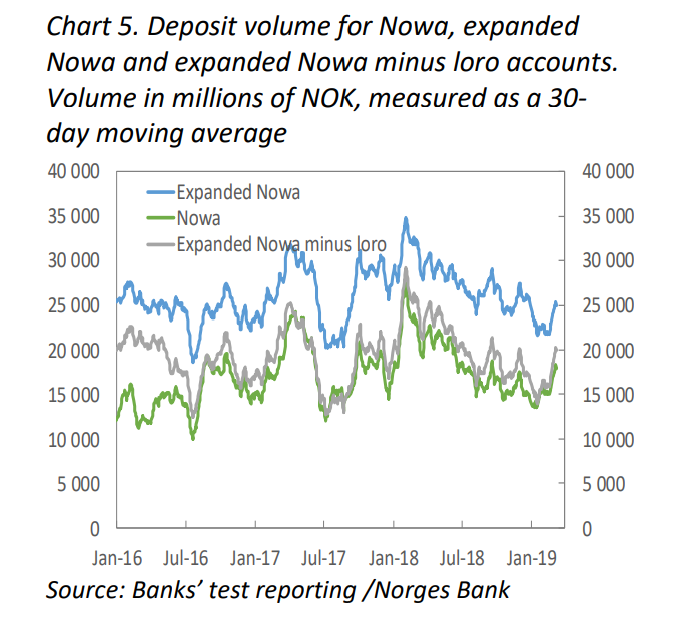

From a quick read of the materials, the key difference between 2020 and old NOWA is how the contingency is calculated. As we saw in our original blog, NOWA has been really volatile around quarter-ends in Norway. The following chart shows that 2020 NOWA should be far less volatile at these (potentially crucial) times:

The “New Nowa” chart-line shows that 2020 NOWA performs much as a true OIS rate should – i.e. it very closely tracks the NOK policy rate.

As we’ve seen with SOFR in the US, volatility of these overnight rates is an unwanted characteristic. Rather than relying on a central bank to step in with smoothing operations, it is nice to see in Norway that a contingency has been defined to fulfill this role instead.

Whaddaya NOWA

In the past 18 months we’ve seen press releases covering the first SOFR trades, the first €STR trades and even some of the first Cross Currency trades in RFRs. You get the feeling that now these transactions are all out in the open on public SDR data anyway (see SDRView!), then the banks involved may as well make a song and a dance about it.

A quick google search for NOWA OIS reveals a first SGD OIS (news to me, well done OCBC and Stan Chart!), but no sign of any NOWA trades yet. Have they happened? Or are we waiting for the first quarter end to make sure that the contingency works on a live rate and the spike isn’t too great? We could surely see a one month tenor transacted before that?

Right Here, Right NOWA

Let’s treat this blog as a call to arms. NOWA has been reformed. The administrator is credible. It even acts like a true OIS rate and closely tracks the policy rate.

It seems everything is in place to start trading NOK OIS right here, right NOWA.