- MXN Swaps are the 8th most traded interest rate swap at CCPs.

- 99% of cleared volumes are at CME, and most MXN swaps are now cleared.

- MXN swaps are a long-dated market. Almost half of all risk is executed in the 5y and 10y tenors.

- 66% of MXN swaps are executed on-SEF, but there is almost no Dealer-to-Client activity on-SEF.

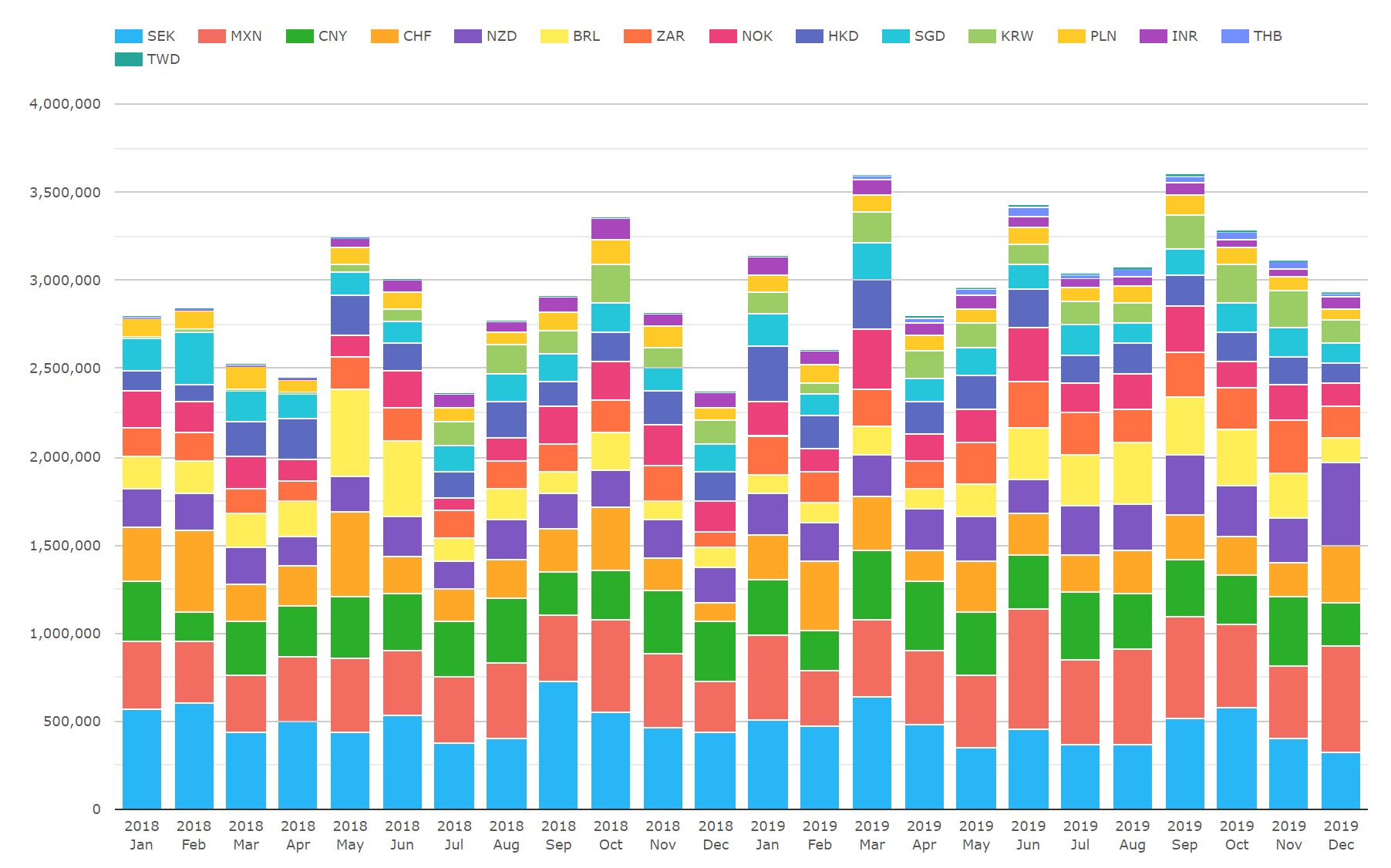

When I took a look at trends in 2019, I found that MXN swaps were the 8th most traded currency in cleared Interest Rate Derivatives.

From CCPView;

Showing;

- Volumes in Cleared Interest Rate Derivatives from CCPView.

- The chart excludes the top six currencies by volumes (USD, EUR, GBP, JPY, AUD and CAD). These six currencies represented over 95% of total cleared volumes (see Four Trends in Swaps Data).

- For the volumes displayed on the chart (not total cleared volumes), SEK represents 16% and MXN 15%.

- The next largest over the last two years were CNY at 11% and CHF at 9%.

I know very little about MXN swaps, so given the high volumes I thought I should educate myself beyond the fact that MXN swaps trade in double the volume of BRL swaps.

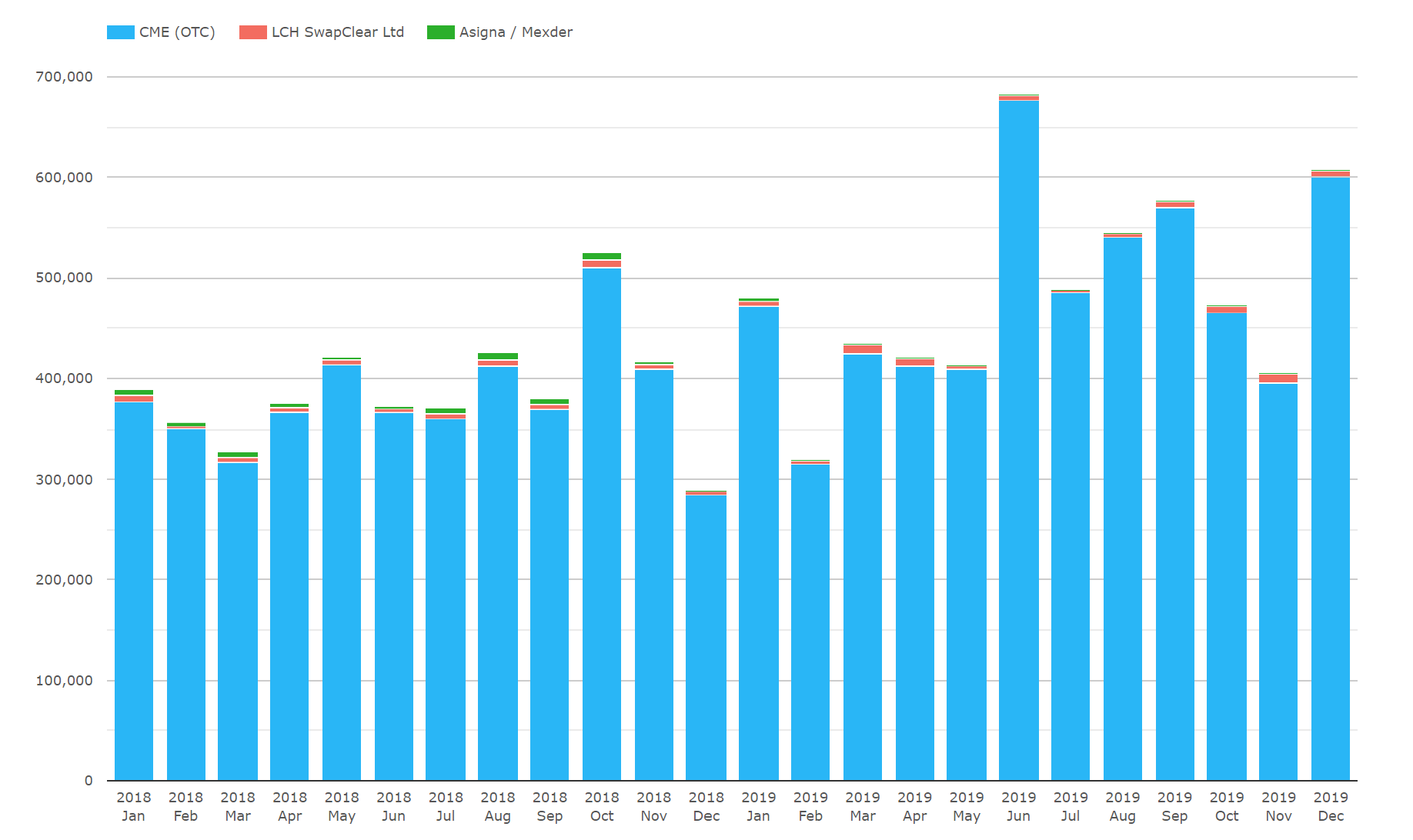

99% of Cleared Volumes are at CME

Whilst we have written a lot about CME-LCH basis over the past few years, we tend to look at CCP Market Share via Amir’s periodic Risk.net articles. So whilst many readers will assume that LCH SwapClear enjoys a commanding market share in cleared swaps, MXN clearing demonstrates that this is not the case across all currencies:

Showing;

- CME have almost all volumes in Cleared MXN IRS.

- Both LCH SwapClear and Asigna also offer cleared MXN, but their volumes are insignificant.

- Whilst cross margining versus other currencies at LCH may be beneficial, it looks like CME benefit from first mover advantage. Recall back in December 2014, there were already MXN cleared volumes at CME.

97% of MXN Volumes are Cleared

In that December 2014 blog, we found that volumes reported to US SDRs were highly representative of the overall MXN market. Is that still the case?

From SDRView;

Showing;

- Total Cleared volumes are much larger than those reported to SDRs. SDR volumes now make up only 56% of total Cleared volumes.

- Almost all MXN swaps reported by US Persons to SDRs are now cleared.

- In the past two years, 97% of volume has been cleared.

On that last point, for those who have not followed MXN markets closely, only ~60% of volumes were cleared prior to September 2016. The first wave of Uncleared Margin Rules accelerated the uptake of Clearing for MXN IRS. There is a good case study on this from CCP12 in their 2018 paper here.

All MXN Swaps are versus TIIE

TIIE is a 28 day index, so a little bit unusual. As a result, swaps trade as a number of periods versus this 28 day period, meaning that the closest to a one year trade is 13×1 (364 days).

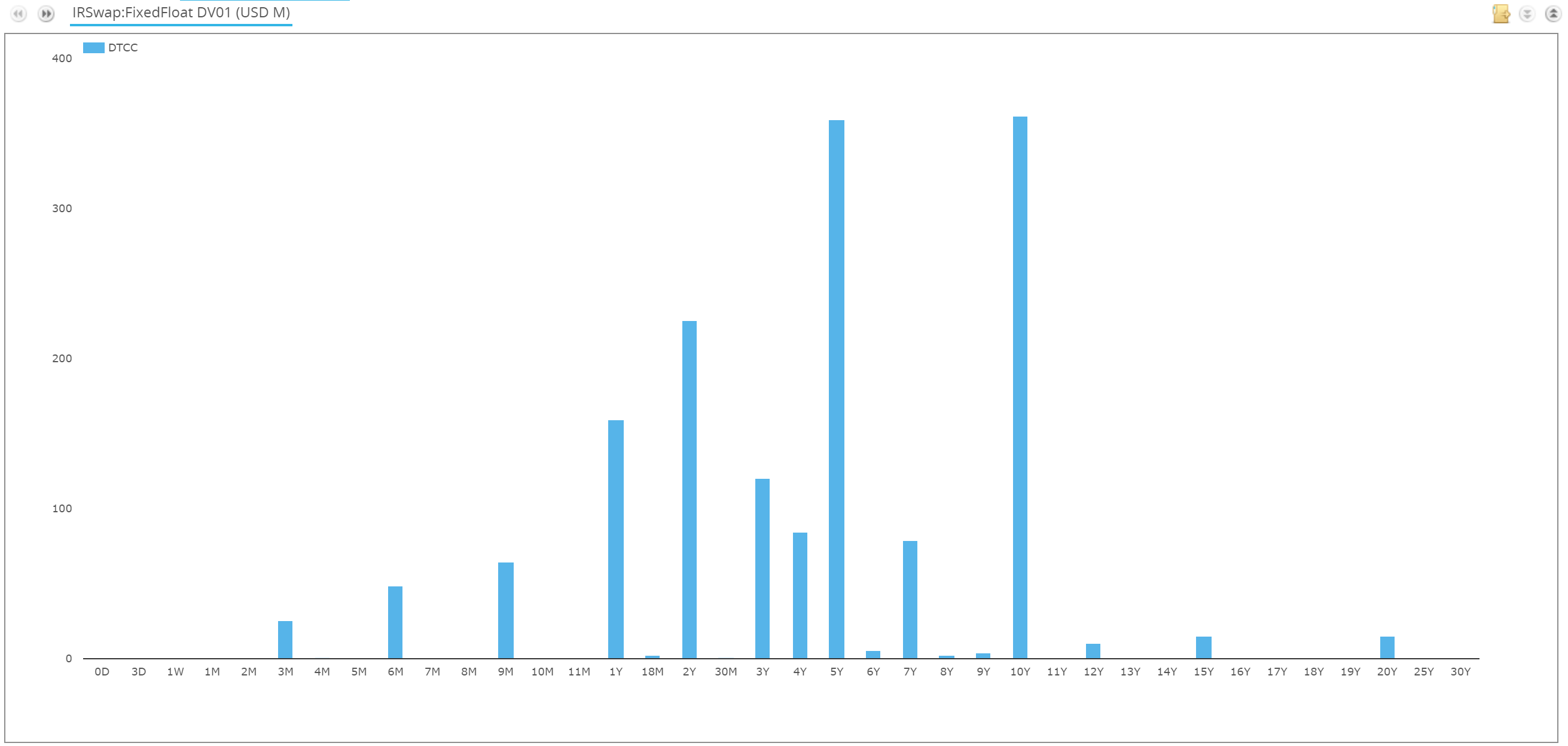

Most Risk is Traded in 5y and 10y

Looking at the trades reported to US SDRs, we calculate the DV01 of each trade and look at the maturity profile over the past two years:

Showing:

- MXN IRS is certainly not a short-dated market.

- In the past four years of trading, 5y and 10y volumes have dominated.

- 46% of the total risk has been traded in these two tenors.

- 2y and 1y are the next most traded at 14% and 10% of risk.

- Maturities traded have been as long as 30y. CME clear tenors out to 31y.

There is no MXN OIS Market

I’ve had a look and I can’t find any MXN OIS indices or trades. Related to this, the rate of interest that is paid on Variation Margin (so-called Price Alignment Interest, PAI at the CCPs) for MXN swaps is calculated as the implied domestic interest rate from tom-next USD/MXN FX swaps, using USD Fed Funds as the base. The CME document here covers this in detail (or see our NOK blog or SGD SOR blog for similar). Will this Fed Funds base shift to SOFR in the future I wonder?

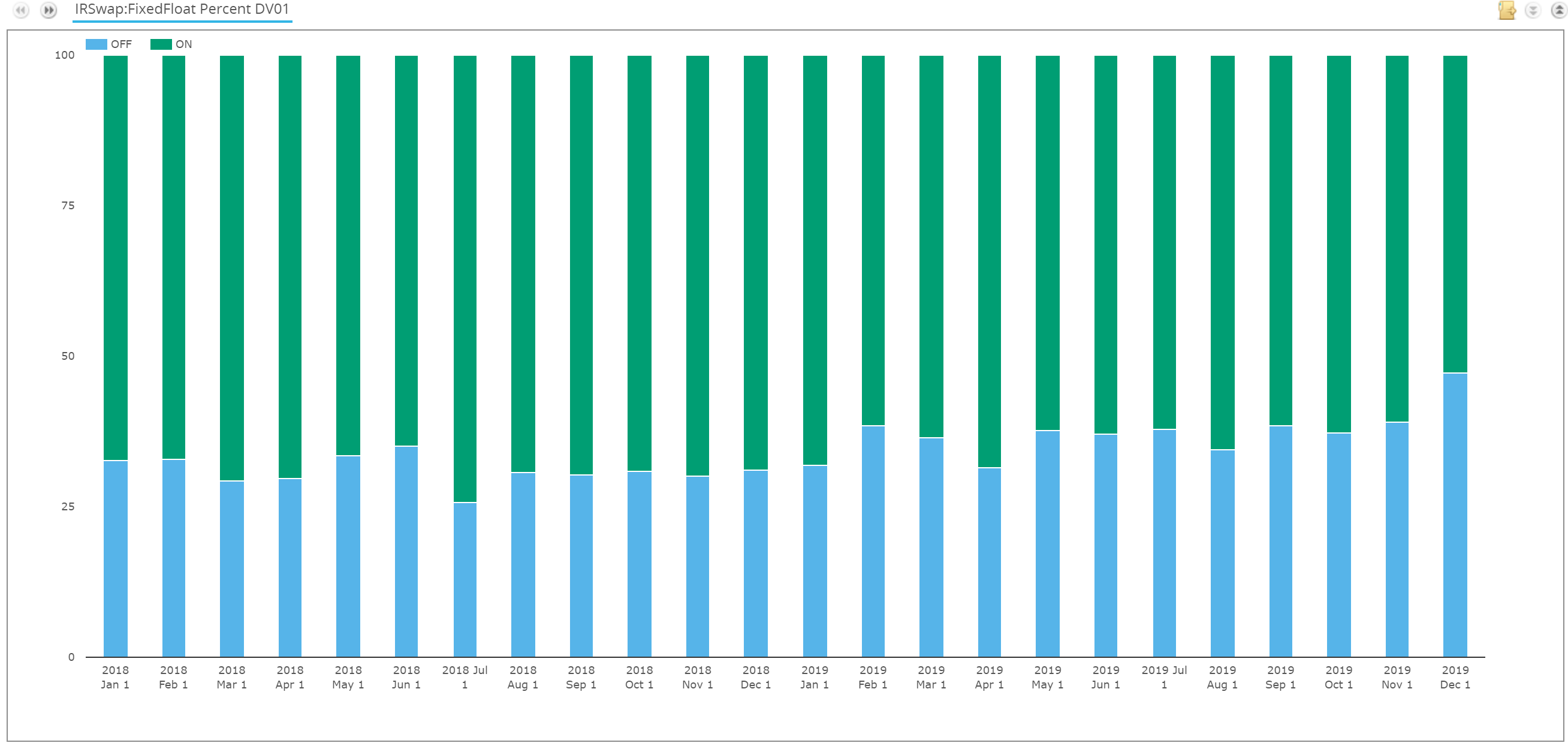

66% of Risk is Executed on-SEF

Finally, we look at how much is traded on-SEF in MXN Swaps. From SDRView;

Showing;

- Nothing much has changed for SEF take-up in the past two years.

- The chart shows the split by DV01 of SEF trading.

- It has consistently been 66% for a good while now.

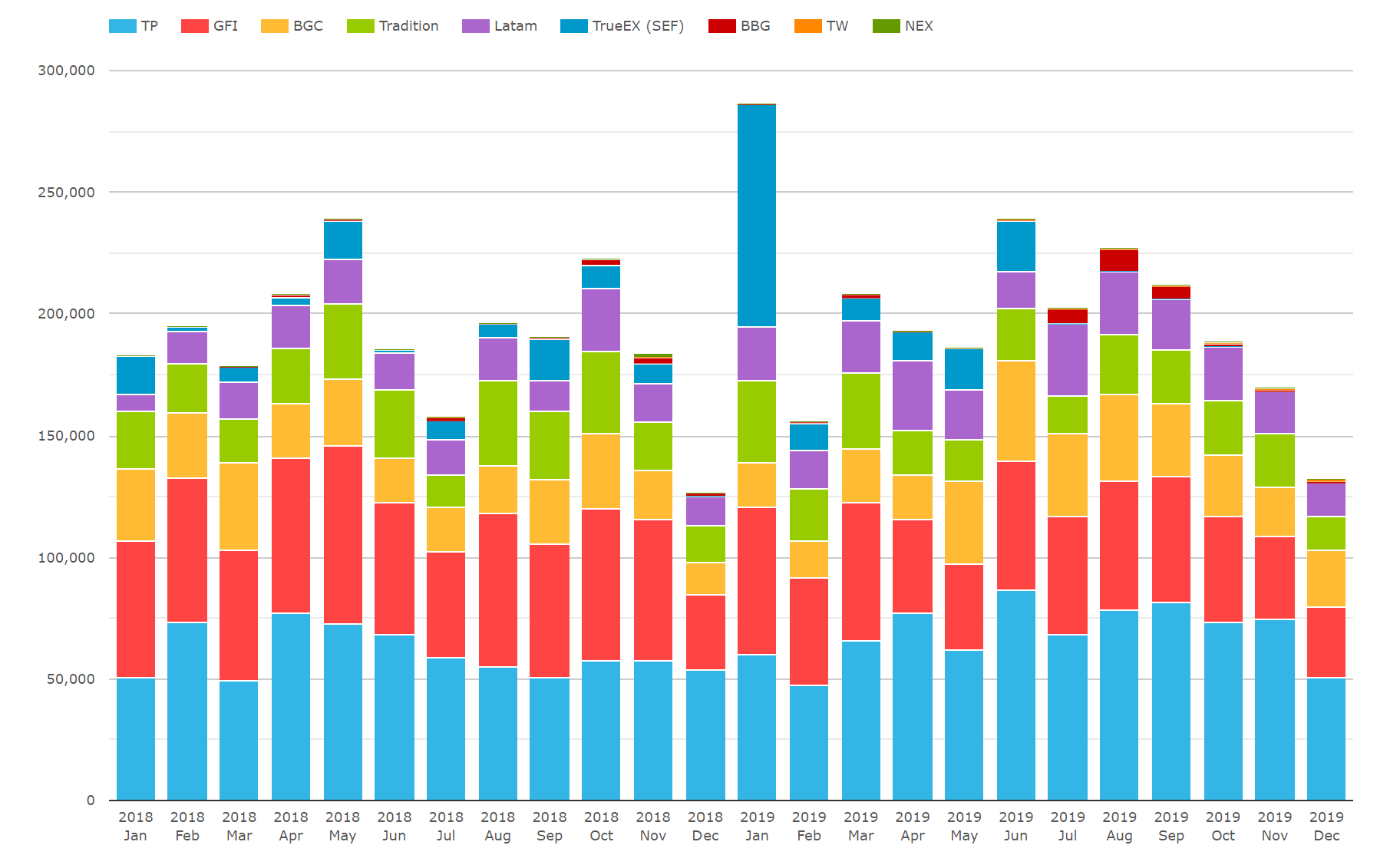

Looking at SEFView, we see the following market share for SEFs:

Showing;

- There are almost no MXN IRS volumes executed on D2C venues such as Bloomberg or Tradeweb.

- The big IDB platforms dominate proceedings, with Tulletts (TP) number one.

- TP have a 33% market share over the past two years.

- GFI are number two at 26%.

- BGC and Tradition are close together at 13% and 12%.

These market share statistics for the IDBs only look at on-SEF MXN activity. Some of the IDBs may have larger off-SEF volumes than others.

In Summary

- MXN swaps are an important market in Interest Rate Derivatives.

- CME enjoy a 99% market share in Cleared volumes for MXN swaps.

- MXN swaps are long-dated products, with most risk being traded in the 5y and 10y maturities.

- SEF trading is popular for MXN, but only on Dealer-to-Dealer platforms.