Is Chris Barnes actually a robot?

Do Androids Dream of Electric Sheep? Amir and I have been discussing on our podcast a new use of the Clarus blog – training AI models. Clarus content is a good candidate for training large language models – the blogs are structured, and they cover technical topics in an accessible manner. There are now well […]

HJM-FMM Model – Fast Calibration via a Neural Network

Authored by, Davide Gianatti, Serena Manti and Gianluca Molteni of the Financial Engineering and A.I. team at List. The aim of this post is to introduce a novel systematic approach that could be used to calibrate quickly any model describing interest rates. The core of the algorithm is a Neural Network (NN) that outputs the parameters […]

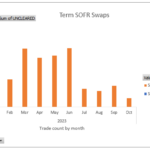

Term SOFR and BSBY Volumes – October 2023

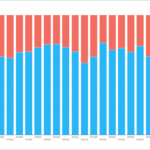

I last looked at Term SOFR and BSBY Volumes in May2023, so today I will look at the YTD 2023 data trends for these indices, and as before seperate Term SOFR (published by CME) from Average SOFR (NY Fed). A one-sentence summary is that “Term SOFR Swap volumes are down, though still far higher than Average […]

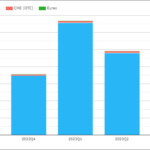

3Q23 CCP Volumes and Share in IRD

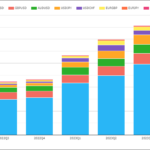

Clarus CCPView has daily volume and open interest data published by each CCP, which is filtered, normalised and aggregated to allow meaningful comparisons of volumes. Today we look at 3Q23 volume and market share in IRD for: Onto the charts, data and details. Volumes and Market Share For major currencies and regions, vanilla swaps referencing IBORs and OIS […]

Is volatility in RFR Adoption here to stay?

Volatility in Rates markets has been elevated this year. However, I cannot remember a year when we haven’t said similar by October! It is very likely that the human-bias is innately more sensitive to change than stasis, which then leads inquisitive minds to work out what is causing the change. But one thing that is […]

Using SACCR to monitor Counterparty Credit Risk

Risk Weighted Assets Counterparty Credit Risk is typically the largest contributor to Risk Weighted Assets (RWAs) for banks. This Clarus blog covered RWAs way back in 2017 when looking at Basel III disclosures. It is highly unlikely to have changed in the intervening six years: In today’s blog, we don’t want to necessarily talk about […]

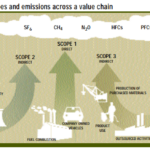

SEC Proposal to Mandate Climate Risk Disclosures

I published an article on the ION Markets Blog, please read at SEC Proposal to Mandate Climate Risk Disclosures. There are differing opinions on whether the SEC has the power to prescribe such extensive rules, a point that SEC Chair Gary Gensler addressed in his recent testimony to the US Senate Comittee on Banking, Housing and Urban […]

Clarus data reveals the truth about SONIA derivatives liquidity

A few weeks ago, I highlighted that the EUR swaps market is now larger in size than the USD swaps market (within a broader blog post on the BRL swaps market): LIBOR cessation is likely the main reason for this change in the relative size of EUR markets. EUR markets trade FRAs and Basis swaps […]

3Q23 CCP Volumes and Share in CRD and FXD

A review of Credit Derivatives (CRD) and FX Derivatives (FXD) volumes and market share at Clearing Houses (CCPs) in 3Q 2023. All the charts and detail from CCPView. Credit Derivatives Volume USD CDX, CDS and Swaptions Overall volumes in 2023Q3 at $3.35 trillion as compared to $3.75 trillion in 2022Q3. Market Share of USD CDX The […]

Clarus Goes Podcasting – What Do You Think?

Amir and I have taken the bold decision to dip our toes into podcasts. For the foreseeable future, we will be giving you a verbal update on the blogs (and what doesn’t make the blogs) once a week. It gives us a chance to quiz each other (in the nicest possible way) about what we […]