What You Need to Know

Last week, the CFTC Chairman, Christopher Giancarlo, presented a whitepaper at the annual ISDA shindig. This whitepaper should be a pretty good guide for any regulatory changes that we can expect to see out of the CFTC for the remainder of his term (it expires in April 2019).

He looked at six areas of market reform (in my order of preference):

- Trade Execution – proposes more flexibility for SEFs so that they do not have to operate an Order Book; expanding the swaps that must be executed on-SEF.

- Trade Reporting – changing regulatory reporting (i.e. non-public) to T+1; change block thresholds and dissemination delays for large trades.

- Uncleared Margin Rules – look at different models (not just SIMM); challenge the 10 day margin period of risk.

- Capital – criticises the Leverage Ratio due to the limited netting under Current Exposure Methodology; encourage use of internal models for calculations.

- CCP Reform – examine the relative sizes of resources within the default waterfalls; encourage more research into these systemic institutions.

- End User Exceptions – re-state thresholds away from notional based measures; continue to provide relief for small banks; don’t make uncleared margin too penal.

Having just read the 100 page document, it is a pretty pragmatic look at the current state of play in US swaps markets from a regulatory viewpoint.

You can see that he is pretty aligned with our Clarus thoughts, particularly when he drops comments like this:

Trading counterparties seek neither the least nor the most regulated marketplaces, but marketplaces that have the right balance of sensible, objective and well-maintained regulation – in other words: good software

“Swaps Regulation Version 2.0” seems like a pretty good agenda to work towards. My only disappointment was that there wasn’t more reliance on the existing data to draw out some of the conclusions. The paper would have been well served to reference the following two charts from SDRView.

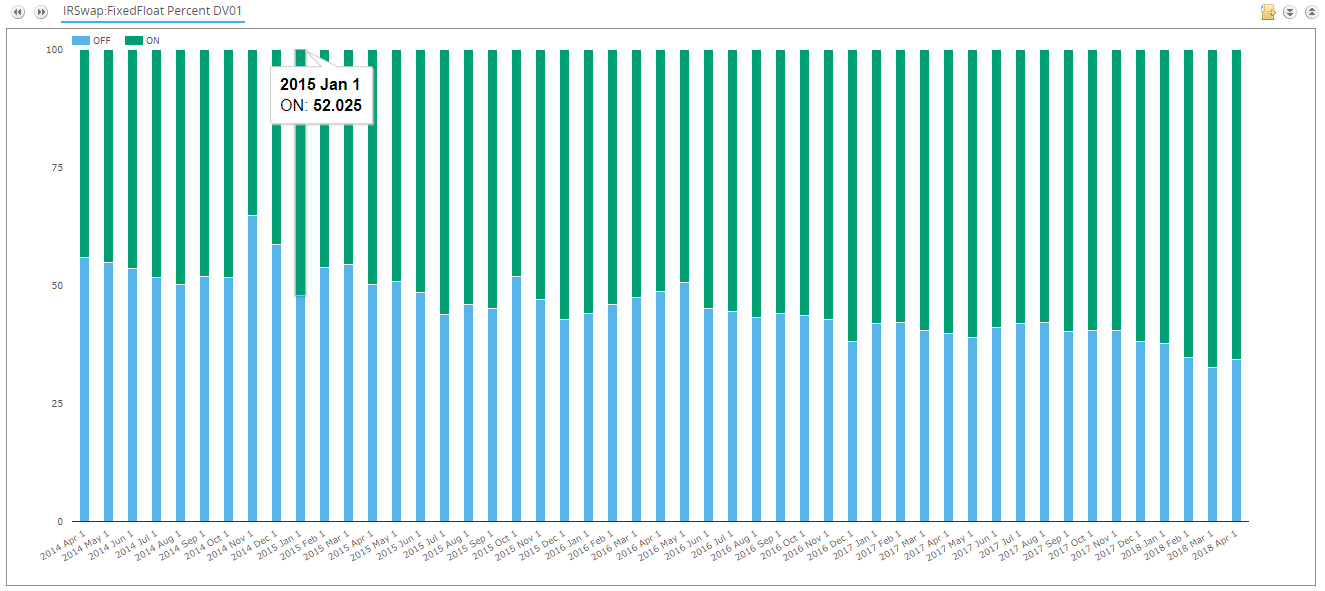

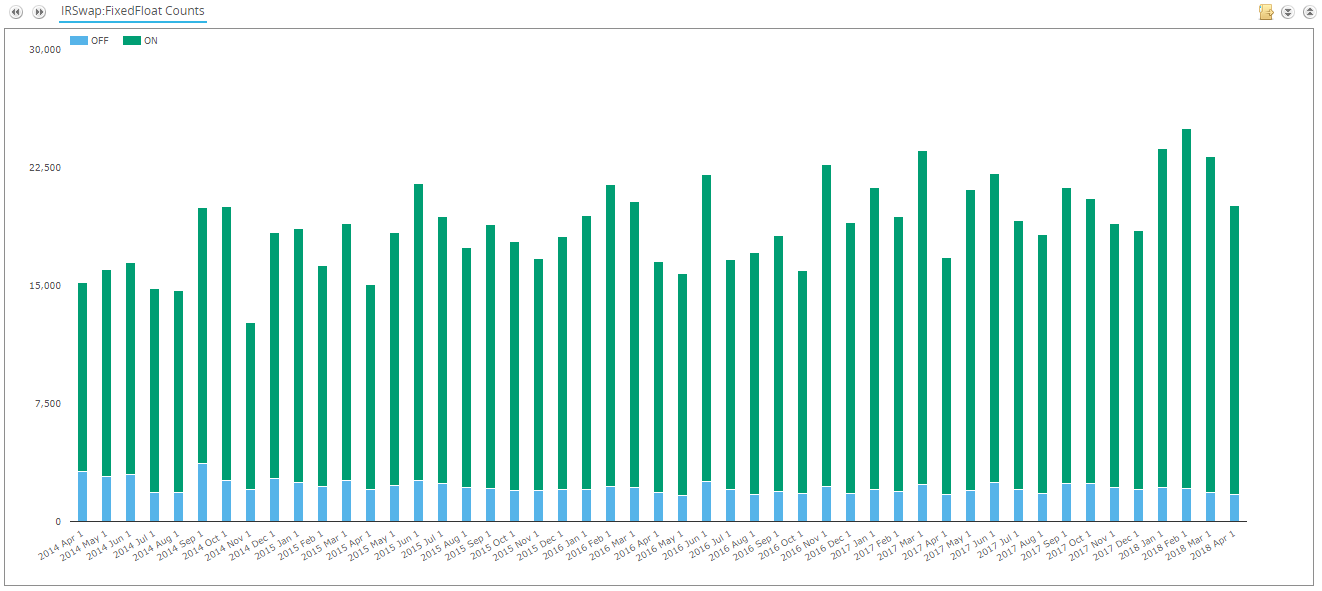

SEF Adoption Has Been Slow Going

SEF trading has increased from 45% to 65% of volumes over the past 4 years (for vanilla fixed float IRS in USD, EUR, GBP and JPY). Most of these volumes are USD denominated. This is the same whether we look at it on a notional or DV01 measure.

SEF trading has increased from 45% to 65% of volumes over the past 4 years (for vanilla fixed float IRS in USD, EUR, GBP and JPY). Most of these volumes are USD denominated. This is the same whether we look at it on a notional or DV01 measure.

From the tone of the paper, the Chairman really wants this chart to look more like the Clearing charts – 98% of these simple, vanilla IRS trades should be done on-SEF. And not just processed on-SEF via an RFQ1 type of workflow, but transacted on-SEF from trade beginning (liquidity and price discovery) through to execution and post-trade processing.

The paper sets out the possible regulatory changes that are required to change how SEFs can transact in order to achieve this.

MAT Trades still occur off-SEF

Further more, the MAT process is pretty confusing and doesn’t match the Clearing Mandate. If SEFs could expand their possible execution methods (but retain and enforce their rules to avoid abusive trading practices whilst maintaining an audit trail), then more products (not just MAT products) could be executed on-SEF.

Going hand-in-hand with this, if all products subject to the Clearing Mandate were also subject to the Execution Mandate, we would expect to see liquidity concentrated on-SEF. It is pretty crazy right now that there remains ~5% of MAT-trades transacted away from a SEF. If the MAT process really worked, these market participants would be motivated to follow liquidity and trade on-SEF and these off-SEF MAT trades (even in block size) would not exist.

Changing the execution protocols that SEFs can offer can (maybe? hopefully?) go a long way to sorting out this situation.

Swaps Reforms 2.0

Onto the paper itself, and our short synopsis. In this week’s blog I will focus on what the paper says about Trade Execution and Trade Reporting. As we have seen with Clarus data over the past five years, both of these reforms have brought true transparency to US swaps markets.

1. Trade Execution

This is really the “biggie” for the paper. It particularly highlights the term “any means of interstate commerce” that became famous in the original legislation.

The goal is to allow SEFs to transact swaps away from Order Books, in any manner that they see fit. All the while, the SEF would still be expected to adhere to its’ existing rules on market behaviour and governance;

For example, such swaps would become subject to SEFs’ rules prohibiting abusive trade practices and to SEFs’ audit trail, surveillance and disciplinary programs.

This seems pretty fair to me. Clarus data shows that Swaps markets do not operate as an all-to-all market at the moment – even with an Order Book Requirement in place. Clients have continued to access liquidity via RFQ to dealers.

The paper suggests:

- Removing the Order Book requirement for swaps that are subject to the Trade Execution requirement. As the paper states, the original Order Book requirement was intended to promote an all-to-all market akin to futures:

The CFTC theorized that this would lead to an all-to-all market where customers could trade directly with other customers by facilitating “trading among market participants directly without having to route all trades through dealers”

- Instead of Order Books, allow for flexible methods of execution that are not limited to just RFQ-3 and Order Books.

This sounds positive to us. But one ask we have is to make sure that the method of execution is made public in the trade report. This is the only way for the industry to positively reinforce good behaviours and be given the right amount of transparency to make that judgement based on real trading.

With flexible execution a given, it then makes sense to suggest eliminating the MAT process. Thus, the CFTC could make all swaps that are subject to the Clearing Mandate also trade on-SEF. This is exactly what the paper suggests.

[This paper] proposes eliminating the requirement that SEFs maintain an Order Book and also permitting SEFs to offer any means of interstate commerce for the trading or execution of swaps subject to the Trade Execution Requirement. In addition, this paper proposes expanding the category of swaps subject to the Trade Execution Requirement to include all swaps that are subject to the clearing mandate. Such expansion would better promote the full range of price discovery, liquidity formation and trading of swaps taking place on SEFs as Congress intended.

The crux of the matter is that we want to see more swaps traded on-SEF and to see more of the lifecycle of a swaps trade conducted within the regulated environment of a SEF. This means bringing the “price discovery, liquidity formation and trading of swaps” onto a SEF.

2. Trade Reporting

There are efforts already underway to standardise data elements of trade reporting, and we are certainly here to assist the CFTC in any way possible with the following aims:

We encourage further research and analysis from industry and academia to assist the CFTC in considering adjustments to public reporting requirements to better optimize trading liquidity with the benefits of transparency in the swaps market.

To make sure that this transparency is as beneficial as possible, the paper suggests looking into three areas of transparency:

Part 45 Regulatory Reporting – This is the data that only the CFTC (and fellow regulators) see. At the moment, it is reported as soon as technologically possible, but it may come in line with e.g. Europe and change to a T+1 basis instead. I can imagine this might make it easier for some reporting entities.

Part 43 Public Data – The paper suggests further research into identifying whether the current blocksizes (and the current 15 minute dissemination delay) are suitable to avoid information leakage for some trading entities. It therefore seems like these may change in the future.

We would just like to state here and now that the different deferrals in Europe are a complete mess and make any meaningful insight into a day’s activity almost impossible until a whole month later. We must avoid this crazy situation where most trades and most volume are treated with a deferral. A deferral should be unusual, not the norm. The current system works pretty well, so we advocate for only minor tweaks here.

DLT efforts – We can’t have a title that includes “2.0” without mention of the blockchain, can we? Public trade reporting seems like a pretty neat use-case where both sides have to verify the data. I do have concerns over how much it would cost to implement (particularly amidst budget cuts). The current system is already the “gold standard” of public reporting when compared to every other jurisdiction, so maybe we should just let the rest of the world catch-up before transitioning to a new system?

Summary

We now look forward to a new, simpler world of SEF execution, without a complicated MAT process. All vanilla swaps should be traded on-SEF via flexible execution methods. This will further aid market transparency and reinforce good trading behaviours. Any changes to public trade reporting in the reforms should be minor, but we would like to see the type of execution method included in the public data.

Next Week

We will outline the suggested reforms to Uncleared Margin Rules, CCPs and Capital requirements in next week’s blog. Stay tuned.