- Brexit has now moved….

- $1.3Trn of EUR and GBP IRS

- $169bn of EUR ITraxx and

- $46Trn of SPS and FRAs

- …onto US-based SEF venues.

Barely a day has passed in 2021 without Clarus receiving an enquiry about Brexit. Our data looking at both where trades are executed and where trades are cleared has been in hot demand this year. We are always happy for people to cite our data, and I have to give particular mention to the below story in IFR that I think is well worth a read:

Let’s kick off and review the data.

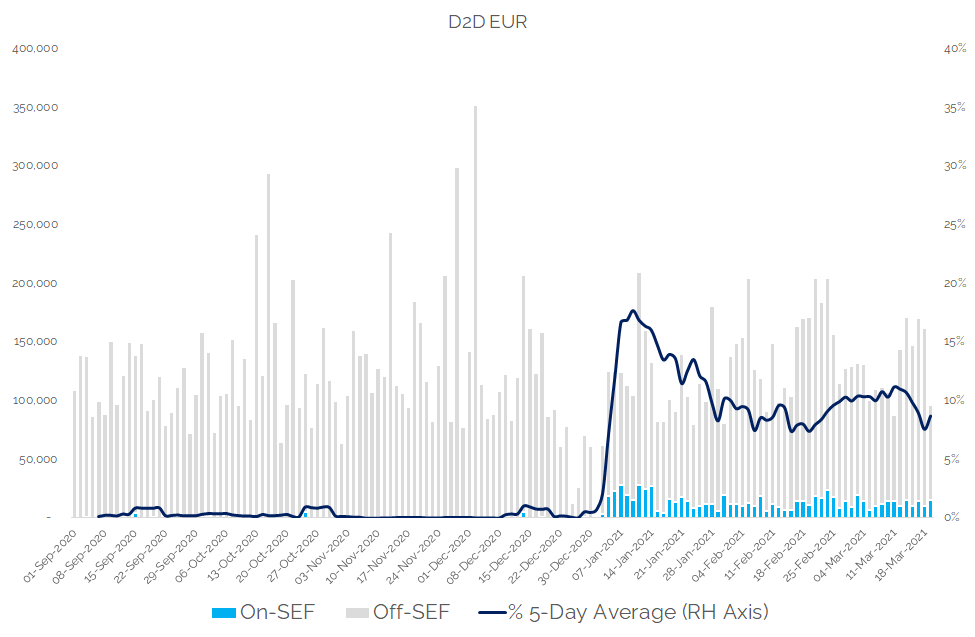

EUR D2D Market

What portion of the global D2D EUR swaps market is now executing on-SEF?

Last time, I stated:

It is notable that the proportion of the EUR D2D swaps market executing on-SEF has now begun to creep back below 10% in recent weeks. Why is this happening and what will the final “steady-state” look like?

US SEFS NOW HAVE 20-40% OF EUROPEAN DERIVATIVES

I think it is safe to say that the chart, with a few more data points shows that:

- ~10% of EUR D2D Interest Rate Swaps now execute on-SEF.

- This is up from basically zero prior to Brexit.

- It has been remarkably consistent since the beginning of February.

The “new status quo” appears to be that 10% of global D2D EUR IRS volumes have moved to SEFs.

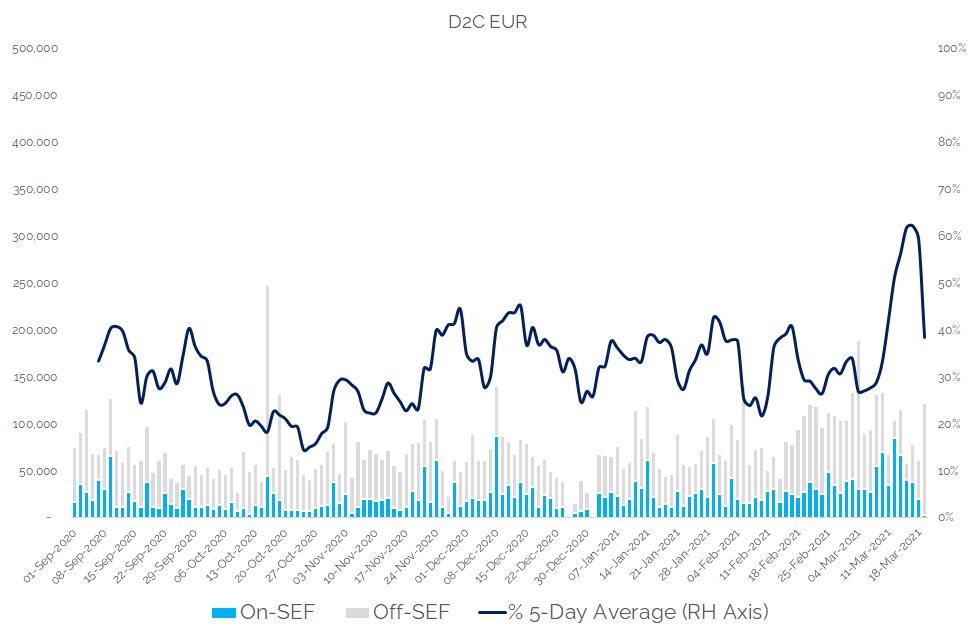

EUR D2C Market

There has been largely no effect on the SEF market for client business. Looking at the market-share of the Tradeweb and Bloomberg SEFs as a portion of the total global client-cleared volumes does not reveal any particular “Brexit effect”:

The spike recently to ~60% of volumes executing on-SEF was driven by very large EUR SEF volumes on 12th March and stands out as an anomaly. On the whole, the average before Brexit was 30%. The average year to date has been 34%. Maybe a touch higher, but it is clearly a volatile time-series.

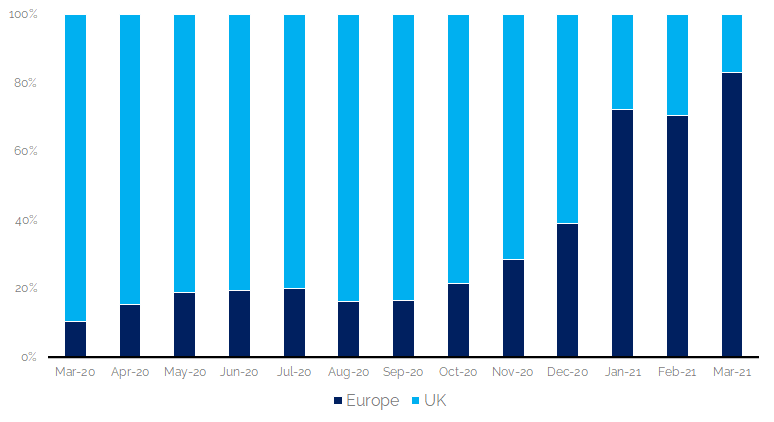

However, one thing has (predictably) changed. Cobbling together the little MIFID-II data that we can in MIFIDView reveals that EUR IRS are now predominantly executed on European-registered MTFs rather than their UK brethren. This has been ramping up since at least March last year:

Showing;

- Percentage of EUR IRS executed on European-registered and UK-registered MTFs as measured by notional.

- The data covers four venues, across two providers, in the D2C space.

- The March 2021 data is largely delayed by four weeks, so take that with a pinch of salt as we only have one complete week of deferred data.

- February 2021 shows a 71% market share for EUR IRS executed on European MTFs versus 29% on UK MTFs.

- This is a significant change from the ~1’% market share that European MTFs had in March 2020.

- However, bear in mind that these European venues are still owned and operated by the same companies who run the UK registered venues.

It remains very frustrating that we do no have decent MIFID II transparency data to perform this analysis more completely. Given programmatic access to the free, 15-minute delayed data we could analyse this trend more completely. It would be interesting to know where trades subject to the DTO are actually being transacted. We continue to have no visibility into the European Dealer-to-Dealer market.

MIFID II data desperately needs to be consolidated across venues to make sense of it. This requires programmatic access to the free, 15 minute delayed post trade data. This is still impossible, 3 years after MIFID II went live. We are losing time and transparency constantly. Need we remind readers that Transparency Helped Derivatives Markets Function During COVID?

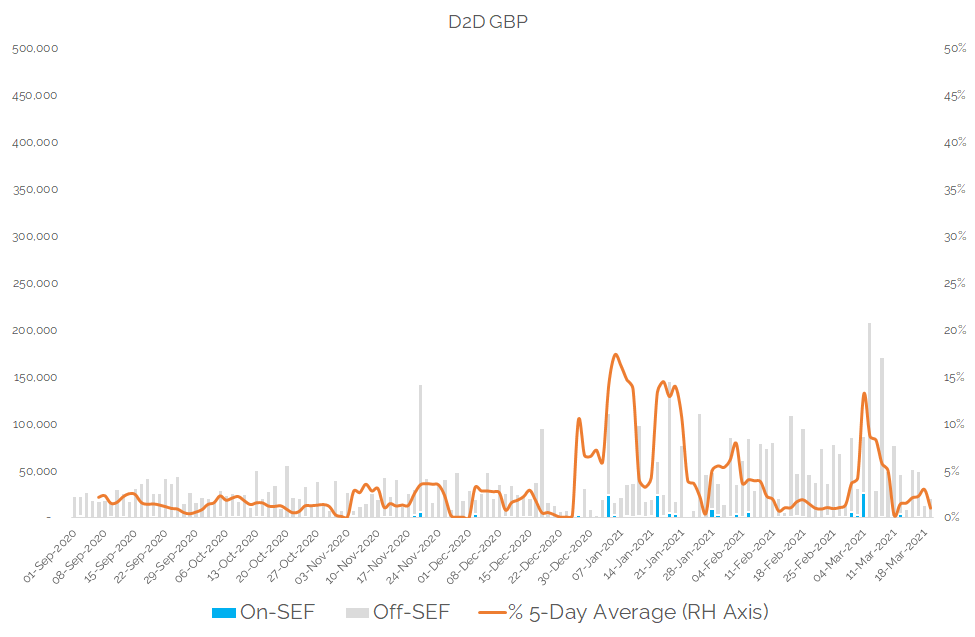

GBP D2D Market

It is somewhat more difficult to interpret the effects of Brexit on the GBP D2D market:

The chart reveals:

- Somewhat irregular volume spikes on particular days in GBP markets.

- Drilling down to trade-level details, these tend to be single period GBP swaps (SPS) trading on the TP and Tradition SEFs.

- Removing these (as we have done for all volumes executed on the NEX SEF) removes these spikes.

- We do not attribute this increased activity in SPS to Brexit, but rather to LIBOR cessation. SPS are compatible with ISDA fallbacks whilst FRAs are not.

Therefore it is more difficult in GBP markets to draw a parallel with what has happened in EUR IRS. A 10% portion of the EUR IRS D2D market has certainly moved to SEF execution. The data only shows that a smaller portion of the GBP IRS D2D market has moved to SEF execution.

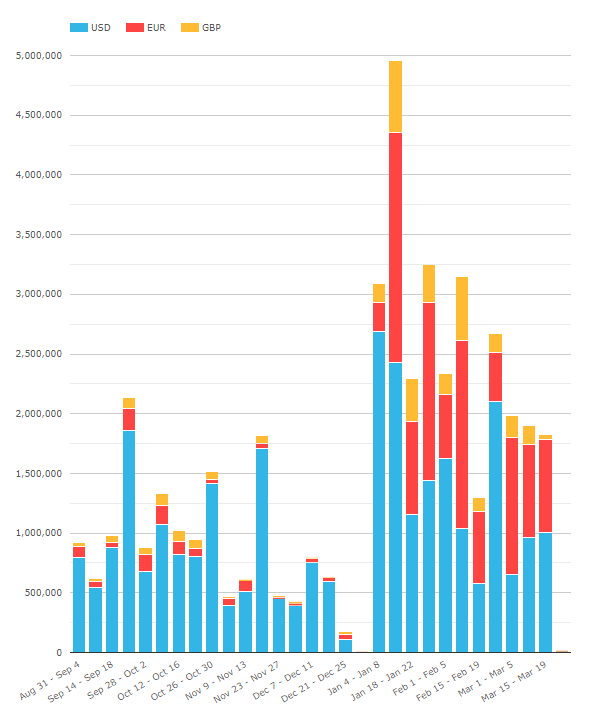

Short End/Portfolio Maintenance Trades Post Brexit

The previous charts, and the IFR article, focus on the day-to-day execution of vanilla IRS trades. However, the largest impact of Brexit has been on where portfolio maintenance trades are executed. Whilst this may be a more technical part of the market (only impacting D2D portfolios as it allows dealers to move fixing risk around), it is nonetheless significant. Across all FRAs and SPS we now see the following volumes executed on-SEF:

Showing;

- Weekly notional amounts executed in USD, EUR and GBP FRAs and SPS on-SEF.

- In Q4 2020, the weekly average notional executed on-SEF for these products was $925bn.

- So far in 2021, this has risen 2.8 times to $2.614Trn.

- In the first two weeks of January alone, >$8trn executed on-SEF in these products.

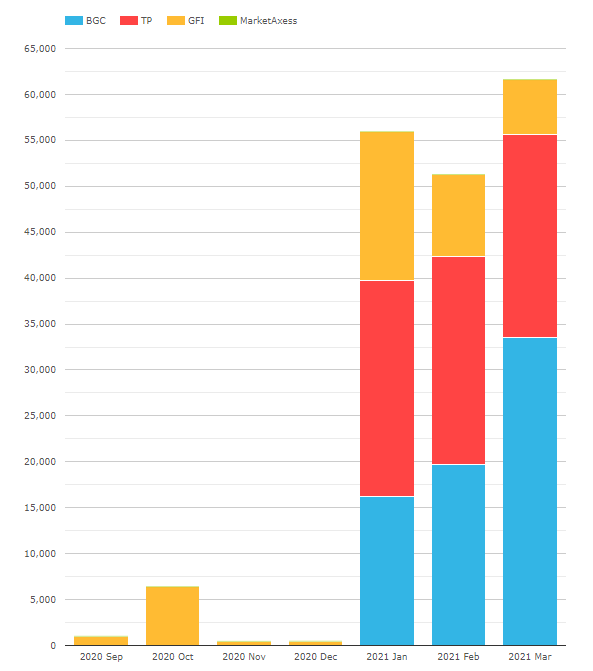

EUR Itraxx D2D Market

The uptake of SEF execution in D2D markets has been starkly exhibited in CDS markets. There were essentially no volumes on D2D SEFs in EUR-denominated CDS products prior to Brexit. These volumes have increased to hit yet new records in the month to date of March 2021:

Showing;

- Monthly volumes of EUR Itraxx index swaps executed on-SEF now stand at $50-60bn each month.

- This has increased from essentially zero last year.

- Beneficiaries are BGC, TP and GFI.

In Summary

- Brexit has impacted where $47Trn of derivatives trades have been executed.

- The beneficiaries are all US-registered SEFs.

- 10% of the EUR dealer-to-dealer IRS market now trades on-SEF. This has been the status quo since the middle of January 2021.

- A smaller portion of the GBP dealer-to-dealer IRS market has also moved to SEF execution.

- Portfolio maintenance trades see an additional $1.7trn every single week executed on-SEF.

- The D2D SEF market for EUR Itraxx CDX has now increased to $50-60bn.