Whilst we continue drafting responses to the pivotal ICE consultation on LIBOR cessation, I have been looking through the data to see how LIBOR cessation is already changing trading behaviour.

Away from the global RFR Indicator, which looks at all linear derivatives, there are certain products that have already been affected. Most notably, the FRA market.

No 2022 FRAs Please!

FRAs are a strange beast. They settle upfront (for GBP FRAs this is also equal to the fixing date) and are discounted at the underlying contract rate, typically LIBOR. They are therefore incompatible with the ISDA Fallback methodology. This is because the payment date cannot be retained on a FRA that has “fallenback” because the fixing using the ISDA Fallback methodology is only known at the end of the period.

However, trading FRAs around the fallback dates is also a strange experience:

- A FRA fixing on the 31st December 2021 will be at a “market” rate. A FRA fixing on the 4th January 2022 (the next business day) will likely use compounded daily RFRs plus a five year median spread. Therefore, whilst a gap of a single business day such as this would normally represent next to no risk, it is now a “toxic” date gap to hedge. What price would anyone show on that?

- Similarly, who in their right mind would trade a FRA starting in 2022 for GBP, JPY or CHF? These instruments are very likely going to have to be either forcibly unwound or physically converted into a Swap product before LIBOR cessation occurs.

- How can existing fixing risk on dates in early 2022 and beyond therefore be hedged?

What is a Toxic FRA?

We define a Toxic FRA as any FRA contract that expires at, around or after, an expected LIBOR cessation date. This contract will exhibit substantial jump risk versus subsequent fixing dates. The contract will likely need to be converted from a FRA into a Single Period Swap at some point (even December 2021 dates may end up being converted to SPS to allow for convexity/discounting hedges versus early 2022 dates).

Is There Any Toxicity in the SDR?

It is therefore fair to assume that any market participants with more than a passing interest in LIBOR (or our blog) would therefore avoid any FRA beginning in 2022 if they really believe that LIBOR will cease being published.

Fortunately, the data from SDRView strongly supports the case that market participants are indeed taking note of the upcoming LIBOR cessation.

We can take the GBP market as probably the best example, given:

- The LIBOR cessation date is the most certain out of all active FRA markets (USD is still up in the air, EUR trades versus EURIBOR, which is continuing for the time being).

- The CHF FRA market is too small to draw any conclusions from.

- The JPY market already trades as single period swaps, a quirk of fate that is turning out to be quite handy in the transition story!

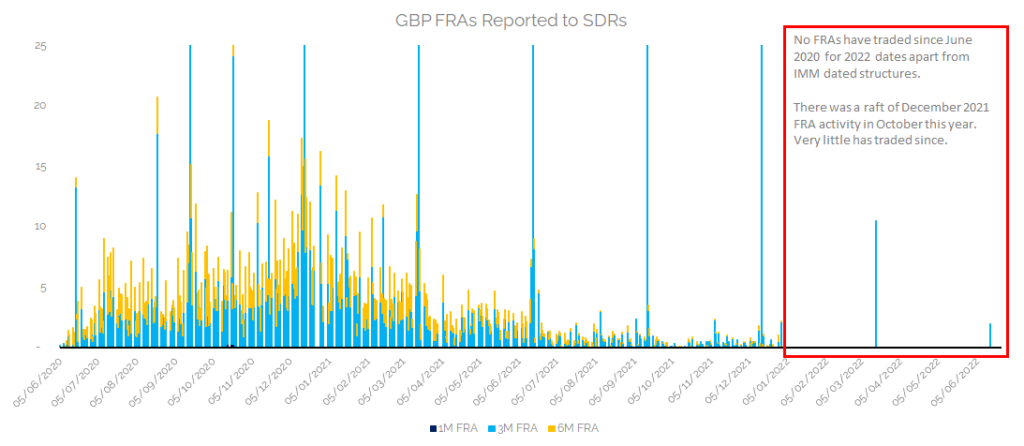

From the SDR data, we can only find examples of IMM dated (Mar22 and Jun22) FRA contracts executed since June this year:

Showing;

- The only toxic GBP FRAs that have been reported to SDRs, i.e. those with a fixing date in 2022, are IMM dated. These could, conceivably, be a play around LIBOR cessation in OTC versus Futures markets. You could design some “interesting” convexity plays around OTC vs futures given the assumption of a flat 25 “DV01” on the futures contract and a FRA converting to an SPS…..

- Crucially, we haven’t seen any 2022 dates submitted from the regular FRA volume matching services. This is a great sign that market participants and brokers are working together to precisely avoid these toxic positions.

- Overall, the volumes transacted in FRAs has significantly declined since early Summer. This can be expected as Rates head lower for longer, but the extent of the volume decline is somewhat surprising.

In terms of toxicity, it is notable that hardly any FRAs expiring in December 2021 have transacted since October 2020. That is about two months where market participants seem to be avoiding these dates. Are they already flat or planning to convert?

FRA Alternatives

ISDA Fallback-compliant structures to hedge short-dated fixing risk already exist. They are called Single Period Swaps and work in an almost identical manner to FRAs:

- A single period swap is a Fixed versus Floating OTC derivative with a Fixed Rate (the agreed price) versus a floating index.

- The floating index can be either a single term (e.g. a 3M LIBOR SPS always fixes versus 3M LIBOR) or it could be compounded overnight rates. The payment periodicity is then a zero coupon, matching the maturity of the trade – there is only ever one payment on an SPS.

- Crucially, where-as a FRA (in most major currencies) is discounted at the fixing rate (i.e. LIBOR) and settled upfront, an SPS does not employ any contract-level discounting. The payments occur at the end of the contract.

The FRA Conversion

It would therefore be sensible, if you wanted to hedge any fixing gaps in 2022, to start using SPS to do so as early as possible.

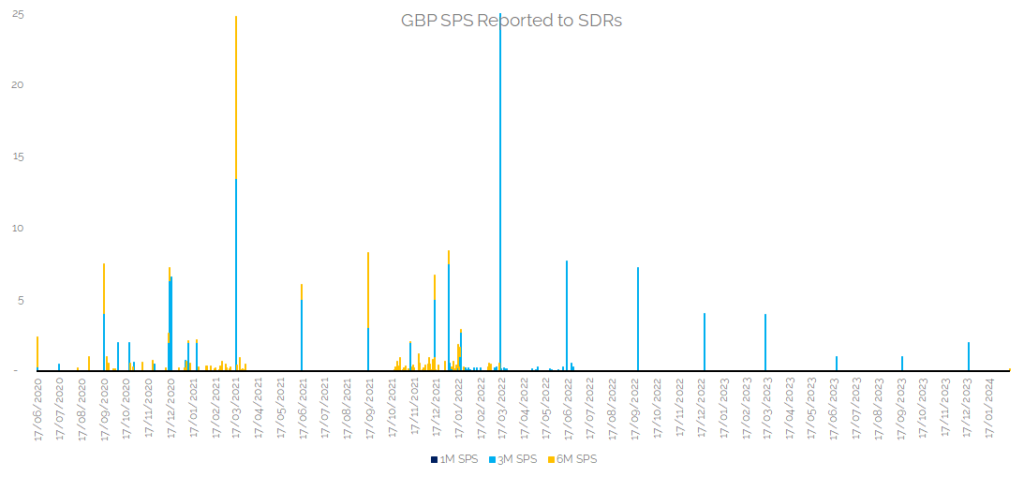

And in the GBP market, we can see that this has been the case (a bit):

Showing;

- About £200bn of GBP SPS have been reported to SDRs since June 2020.

- Many of these SPS are clustered around dates from November 2021 to March 2022.

- The largest activity is on IMM dates (as it is for FRAs).

However;

- FRAs are continuing to trade for short-dates, expiring before December 2021. As recently as December 8th and December 15th 2020, we see volume matching runs sending GBP FRA positions to the SDRs.

- There is therefore a current preference from market participants to continue trading FRAs rather than SPS.

Capital Implications of FRA -> SPS Conversion

Many thanks to our readers who have explained the following to me, as I do not think it is obvious at all.

One of the main reasons that the market has not just switched, without thinking, from FRA trading to SPS is the following:

- A FRA that fixes 9 months for now is treated as a sub one year product for purposes of Leverage and GSIB calculations under the Current Exposure Methodology. It therefore carries a 0% risk weighting.

- An SPS that fixes in 9 months times is treated as a one year product for Leverage and GSIB, and therefore attracts at 0.5% risk weighting!

Same product, almost identical risk profile, and yet if a trader were to convert their FRA portfolio to SPS before year end 2020, they will end up with a capital hit (depending on jurisdiction) but most importantly a GSIB hit relative to their peers!

So I can largely see the FRA to SPS conversion being a 2021 job (as it would be preferable to convert the whole portfolio), but I have no idea where that leaves FRAs expiring in October-December 2021. I guess by year-end 2021 it won’t matter whether they are SPS or FRAs for GSIB purposes….

The GBP FRA to SPS Transition

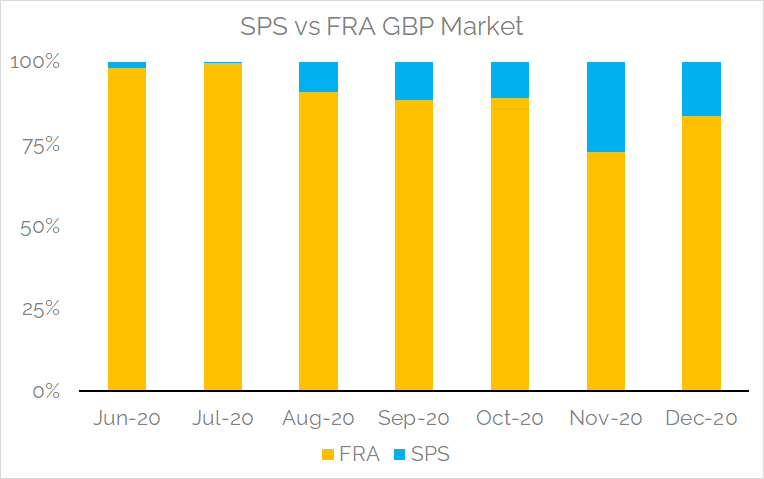

Finally, it is worth noting that SPS are becoming a larger portion of short-end products reported to SDRs and this seems to be increasing. Looking at the ratio of FRAs to short-dated SPS volumes:

Showing;

- At the beginning of 2020, almost no GBP SPS were reported to SDRs.

- In November 2020, 27% of short-dated risk was transacted as an SPS.

- This process may well increase in Q1. The transition to GBP SPS as the market standard could well be completed in Q2 next year.

Crucially, we still think the transition to SPS has a long way to go in GBP. There is much more evidence of IMM-dated SPS in GBP rather than SPS being used to hedge fixing-date mismatches. Volume-matching SPS runs still look to be in their infancy.

A Transparent Transition

Finally, we continue to be thankful for the level of market transparency afforded by post trade transparency in the US. It wouldn’t be possible to pinpoint these changes in market structure without it.

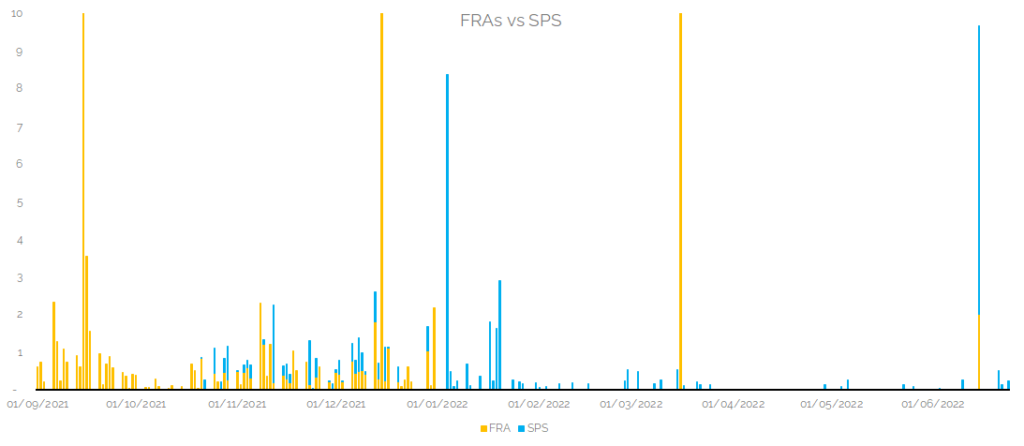

A great example of the use of this post-trade transparency is looking at how GBP FRAs simply stop as at December 2021 and virtually all 2022 volume has been in SPS:

Two things to note:

- To really assess the GBP transition, we would love to be able to add European transparency data to this story.

- I wonder what the data in USD looks like?! One for another time perhaps….

Finally, I will take the opportunity to wish all of our readers a very Merry Christmas and thanks for reading in 2020! See you in 2021….