In a quick blog today I summarise a recent report from the FICC Markets Standards Board about execution analysis in our markets. And suggest a potential way forward…

The Who?

First off, it is worth highlighting the role the FMSB intends to play in our markets:

In their own words:

The Fixed Income, Currencies and Commodities Markets Standard Board (FMSB) is a standards setting body for the wholesale fixed income, currencies and commodities (FICC) markets.

From their rather fancy website here

Anyone familiar with the Clarus blog and our data products will see that we share a lot of the same space after a brief perusal of their latest papers:

They manage to tick off RFRs, data management, block trades and execution quality in the past 12 months. All of those were hot topics on our blog, ranging from the ISDA-Clarus RFR Adoption Indicator, to our Block Trading consultation response and of course all of our data products!

Measuring Execution Quality in FICC Markets

The report that grabbed my attention this week was first published back in September 2020 (whilst the rest of us were still trying to work out what happened in the March volatility I think!). It is called “Measuring Execution Quality in FICC Markets“.

Transaction Cost Analysis

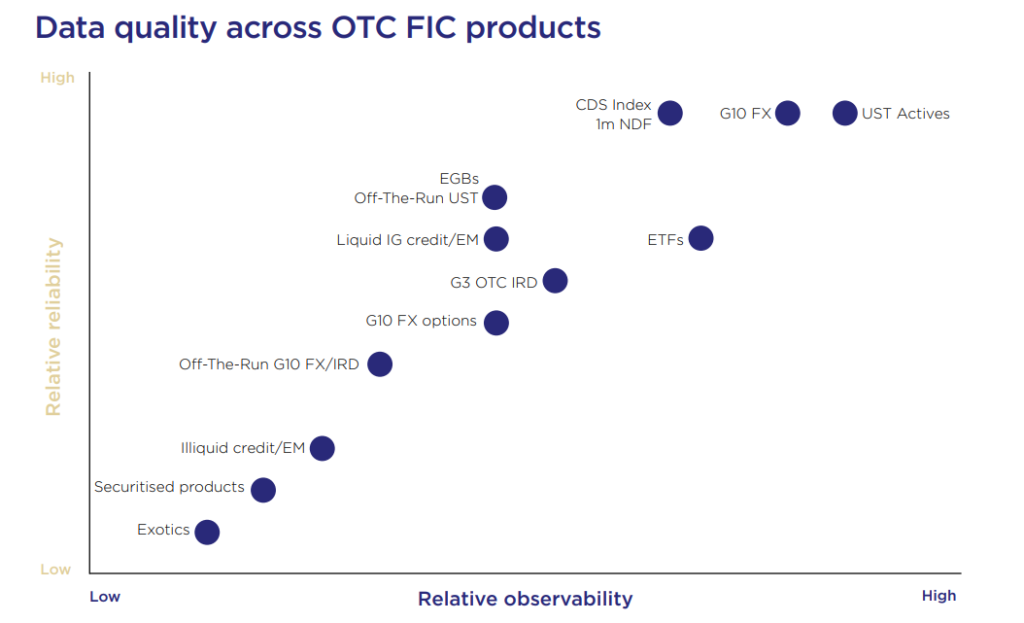

A use case that is often posited to us regarding the Clarus post-trade data is how it can be applied to Transaction Cost Analysis/Best Execution assessments. When you look at the high-level availability of data for Interest Rate Derivatives, it looks like this should be eminently achievable:

Where G3 OTC IRD is bang in the middle, with “average” ratings for both the reliability and observability of data.

However, the FMSB report quite correctly identifies that OTC Rates markets are still “episodic” in nature. They are defined by irregular, large-sized trades transacting. There is therefore very little chance to create a public tape of continuous post-trade prices for these instruments under the current market structure.

Of course, that does not preclude the possibility of trading venues providing continuous prices as a pre-trade price feed. When we talk about the reliability and observability of price data in OTC Rates markets, these (relatively expensive) sources would be the go-to resource, as opposed to post-trade data.

In terms of using post-trade data for any element of execution analysis, we are particularly hamstrung by the inaccessibility of MIFID II data. The FMSB fairly highlights this as a problem in terms of achieving a whole market view. In particular they highlight ESMA’s own December 2019 assessment of the MIFID II regime, in which ESMA conclude:

Obstacles

The report correctly identifies elements of the OTC Rates infrastructure that make it unsuitable/extremely difficult to create a transaction-based assessment of execution quality even for a vanilla swap:

- Dealers and Customers continue to execute in separate pools of liquidity. Nowhere is this better evidenced than Clarus SEFView where the share between D2C and D2D venues is a frequent talking point!

- Trades are episodic. There are long intervals during the trading day where no trading takes place, then a single trade can activate a bunch of activity. Whilst we have had success in creating continuous pricing streams for something like USSW10 (spot starting 10 year USD swaps) from US post-trade data alone, we don’t see enough transactions in other OTC Rates products to produce similar. However, work from BoE researchers suggest this should be possible for EUR (and maybe GBP) swaps if using LCH data, for example.

- That doesn’t necessarily help in assessing the execution quality of a non-standard trade however. The whole OTC market is predicated on the ability to trade customised structures. These should not be exempt from execution analysis just because they are (slightly) modified from market standard.

- D2C trades RFQ whilst D2D is more akin to a Central Limit Order Book, albeit stopping well short of a “lit” equities CLOB. Should there be different measures of execution quality depending on the method used?

A Path Forward

It is not the place of the FMSB paper to suggest solutions for this, but rather a series of standards for the market to look to get behind. You can read these for yourselves on the final page of the report (under Best Practices here).

For me, applying some pragmatic ideas in Rates OTC land, I would suggest the following is pretty sensible from an end-users perspective:

- If you are transacting in market-size, is there really any harm in performing an RFQ to three dealers? Particularly if you do not disclose the directionality. Isn’t comparing 3 quotes on the exact transaction at the time of execution the single best way to evidence quality execution (best price wins?). There are subtleties around who the RFQs should go to of course, but let’s assume we are not trying to game the system from day one.

- If you are transacting above market size, you may not want to let that information leak around the market. Therefore, you may be motivated to ask only one dealer. How do you know they have given you a fair price for these large trades, which are arguably the most important trades from an execution perspective? I would argue a survey-based methodology is a pretty good substitute.

How would the survey work? Once a month, dealers are surveyed as to how far from mid they would quote 10Y USD swaps in $50K, 100K, 200k and 500k DV01. This gives an indicative margin from mid for most sizes of trade. If the RFQ response is within those parameters, you are probably getting a fair price.

Now this is easy to pick holes in. Dealers would be motivated to quote large margins on the survey. What if a dealer is axed and would actually be willing to fill your order at mid at the point of execution etc. All of these things can be policed. The larger barrier is getting the survey responses in the first place!

Fortunately, someone like the FMSB should be well placed to put something like this in place…..