Cross Currency Swap conventions in an RFR world

In January 2020, the ARRC published the final recommendations for cross-currency swap conventions. It should be noted that the recommendations are primarily directed towards dealer-dealer trades and the publication points out that dealer-end user trades may require different structures. I have commented previously on potential options in AUD markets and more generally for other currencies. […]

Swaps Data: Record Trading Volumes in March

My monthly Swaps Review looks at cleared volumes in the most recent 3-month, covering Volumes Feb-Apr 2020 compared to Feb-Apr 2019 Interest Rate Swaps in USD, EUR, JPY Credit Default Swaps FX Derivatives (NDF, FXO) CDS was the standout with almost twice the monthly volume in March 2020, while USD IRS and NDF both achieved […]

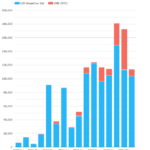

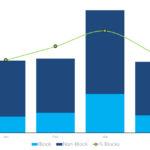

CFTC Block Trading Consultation May 2020

Our analysis shows that more blocks transacted than ever before in March 2020. More volume traded as a block on-SEF in March. There is no difference in Price Dispersion between block and non-block trades during both normal and stressed market conditions. The current 15 minute delay in reporting for block trades has no negative impact […]

How Much Margin? 2019 Edition

We analyse how much Initial Margin is being held versus derivatives in 2019. This covers cleared and uncleared OTC derivatives, plus exchange traded contracts (Futures and Options). It is difficult to perform the same analysis for Variation Margin. We take a look at the latest ISDA Margin Survey to see if it holds the answers. […]

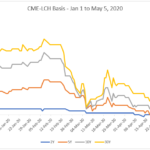

CME-LCH Basis Spreads Turn Negative

We last looked at CME-LCH Basis in August 2019 in CME-LCH Basis Narrows to Four Year Low and as there has been significant volatility in the last few months, high time we looked at this again. Background For Swaps that are economically the same, it is non-intuitive that the fixed rate should be different depending […]

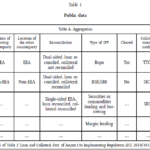

SFTR Reporting – Public Data

For some time now I have been noting, but not reading, articles about the Securities Financing Transactions Regulation (SFTR) being implemented in Europe, so today I wanted to take my first look into this regulation. Background The ESMA website has a good section on SFTR Reporting, so I will copy & paste liberally from that, […]

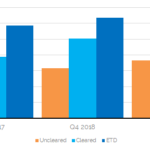

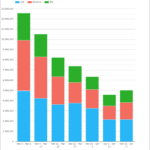

US Treasury Volumes and Market Size

Post-trade transparency in US Treasuries has arrived. CCPView now includes volumes across US Treasuries, Futures and Swaps. This reveals that the true size of the Rates market in the US is $12.5 Trillion per week in notional equivalents for medium and long-dated interest rate products. We can also monitor the split of trading across different […]

The GSIB Framework and Window Dressing

What Are GSIBs? If you need a refresher of the GSIB framework, please check-out our blogs on: G-SIB MECHANICS AND DEFINITIONS G-SIB SCORES FOR US BANKS We have recently introduced GSIBView, an app for analysing the scores in more detail. It provides a drill-down into the GSIB components and allows our data customers to analyse […]

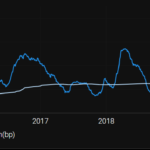

What has happened to USD LIBOR Fallback Spreads?

The fallback spread is an essential component of the LIBOR cessation plan and represents the credit and liquidity component of LIBOR relative to Risk Free Rates (RFRs). In a case where a benchmark like USD LIBOR ceases to publish, fallbacks such as compounded SOFR plus the spread are used to replace the failed benchmark. ISDA […]

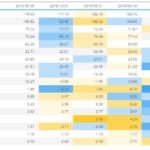

Central Bank Responses to COVID-19: FX Swap Arrangements

We detail the FX Swap lines offered by several central banks to supply their local markets with USD. For the mechanics of how the USD trades work, please see our previous blog. In this blog, we look at the usage of the FX Swap Lines per central bank. Volatility Markets remain in crisis mode. This […]