SOFR First – LIVE Blog

Good morning, happy Monday and welcome to SOFR First day! SOFR activity accounted for 18% of the market (18:30pm London time). Today, Monday July 26th, is when a global initiative coined “SOFR First” comes into play for interbank markets. As per the CFTC MRAC announcement two weeks ago: SOFR First represents a prioritization of trading […]

Clearing Mandates and new Trading Obligations – regulatory change is happening.

The UK and Europe are currently consulting on both the Derivatives Clearing and Trading Obligations. Clarus are worried that the UK consultations risks a significant loss of transparency to markets. Particularly for USD. There appears to have been silence out of the CFTC on these important subjects. Europe has proposed covering some RFRs in the […]

Is RFR Trading Now Ready for Lift-Off?

We are 12 days from SOFR First. 12 days from the point that interdealer markets plan to switch to trading SOFR instead of LIBOR as the market standard. The CFTC yesterday officially adopted the SOFR First recommendations at the Market Risk Advisory Committee meeting. We are 12 days away from interdealer swaps “prioritising” SOFR first […]

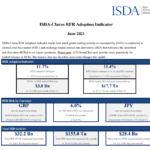

10.7% of New Risk Traded versus an RFR

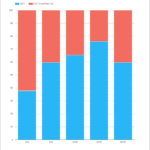

The latest ISDA-Clarus RFR Adoption Indicator has been published for May 2021. It saw an increase to 10.7%, a small increase from last month. When will the big leaps happen? Showing; The RFR Adoption Indicator was at 10.7%. This was higher than last month and very similar to all of the 2021 readings (March aside). USD SOFR decreased to […]

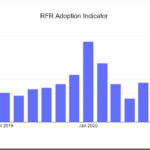

New: What caused volumes to decrease in April?

The latest ISDA-Clarus RFR Adoption Indicator has just been published for April 2021. It saw an increase to 10.1% and it is now back to the levels it has been at for most of 2021. Was March maybe just a blip in the RFR story? Showing; The RFR Adoption Indicator was at 10.1%, higher than last month […]

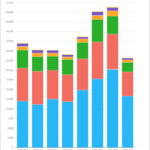

JSCC and CME RFR Adoption Indicators

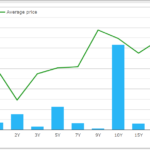

A client recently asked us if we had ever calculated our RFR Adoption Indicators for individual CCPs. The answer was a surprising “No” so I thought I should rectify that in today’s blog. This was somewhat motivated by this Risk.net story on JPY this week. The story highlights how different CCP market shares are at […]

What happened to reduce RFR trading?

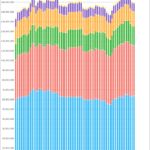

March 2021 saw 8.8% of all derivatives risk traded versus an RFR. This reduced from the previous levels around 10%. The pre-cessation announcements last month do not appear to have accelerated RFR Adoption. There was an increase in the amount of IBOR-related activity last month. Overall for Q1 2021, the total amount of RFR activity […]

Potential challenges of a synthetic LIBOR

Most active market participants were looking forward to the LIBOR cessation or pre-cessation announcement to provide certainty for the end of LIBOR. This was provided by FCA on 5th March 2021 as a pre-cessation or ‘loss of representativeness’ announcement which triggered many contracts to move to the fallbacks at a future date. However, another component […]

LIBOR LIVE – Is GBP LIBOR now dead in derivatives?

Will today be Day One of the LIBOR end game? It should be, according to the latest “Dear CEO” letter from David Bailey, Sarah Breeden and the FCA: ‘Transition from LIBOR to Risk Free Rates’. The end of Q1 2021 is meant to have signaled the last day for business as usual linear GBP derivatives […]

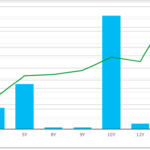

SONIA is now the Benchmark Rate in GBP Markets

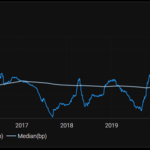

February 2021 saw 10.6% of all derivatives risk traded versus an RFR. This has now been stable around 10% for some time. We cover the pre-cessation announcements concerning LIBOR and the historic spread calibration that took place last week. There has also been a sharp move higher in the amount of long-dated SONIA risk being […]