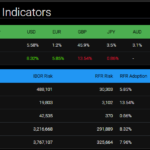

Monitoring your own RFR Adoption Indicators

Last summer I wrote Calculate Your Own RFR Adoption Indicators to explain why it was important on IBOR Transition projects to benchmark and monitor your own firms adoption rate versus the market. In a nutshell, your project needs to know if your firm is lagging, leading or in the middle of the pack and respond […]

SOFR Futures and Swaps – Feb 2021

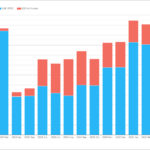

February 2021 was an interesting month in interest rate markets with the volatility in US Treasuries showing up in many products. Today I look at what happened to volumes in derivatives referencing SOFR. Volume and Open Interest in SOFR Futures Volume and OI in SOFR Swaps SOFR Swaps at US SDRs SOFR Swaps on SEFs Clarus Data provides […]

Did You Know That The New Amount of SOFR Risk Hasn’t Changed for 3 Months?

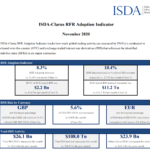

The latest ISDA-Clarus RFR Adoption Indicator has just been published for January 2021. It is quite incredible how stable it has been recently. The overall Adoption Indicator was again at 10.0%, identical to December 2021. This means that 10.0% of all of the derivatives Rates risk transacted during January 2021was versus a Risk Free Rate. […]

3 New Fed Fund Charts You Need to See

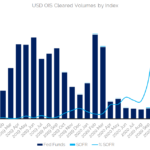

$2.5trn in OIS swaps versus Fed Funds were executed in December 2020. This compares to $364bn for SOFR OIS. We run through the data for the global market, the US market and the basis swap markets. As we continue to compile data for our response to the IBA Cessation of LIBOR consultation, a natural question […]

Toxic FRAs, Fallbacks and Single Period Swaps

Whilst we continue drafting responses to the pivotal ICE consultation on LIBOR cessation, I have been looking through the data to see how LIBOR cessation is already changing trading behaviour. Away from the global RFR Indicator, which looks at all linear derivatives, there are certain products that have already been affected. Most notably, the FRA […]

Libor pre-cessation announcement – how wrong was the market?

In November I looked at the risk implications of a LIBOR pre-cessation announcement which was widely expected in December 2020. Basis markets such as SOFR/USD LIBOR and SONIA/GBP LIBOR clearly priced the spread to be fixed at the announcement in December (i.e. over the next month or so) and that the fallbacks would take effect […]

RFR Trading November 2020

The ISDA-Clarus RFR Adoption Indicator has been published for October 2020. The headlines are: The RFR Adoption Indicator was 8.3%, a decline from the previous month (which saw an all-time high). This is the fourth highest reading on record. 5.6% of all USD risk was traded in SOFR vs 9.7% last month, reflecting the impact of the CCP discounting change. The switch to […]

Will anyone trade LIBOR after 2021?

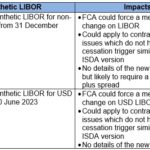

US regulators have announced that banks should cease entering into any new contracts referencing USD LIBOR from 31st December 2021. This is consistent with the announcement last week from the UK regulators, who pointed out that LIBOR fixings may be published after end-2021 but that no new business could be written against them. These announcements […]

ISDA-Clarus RFR Indicator: SOFR, So Good

The ISDA-Clarus RFR Adoption Indicator has been published for October 2020. The headlines are: The RFR Adoption Indicator hit 11.6%, a new all time high. This was up from 10.5% the prior month. 9.7% of all USD risk was traded in SOFR vs 5.8% last month, reflecting the increase in SOFR activity as a result of the CCP discounting change. […]

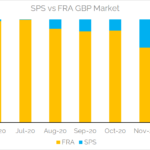

Libor pre-cessation announcement – risk challenges for non-cleared derivatives

In August I looked at the potential for valuation challenges as for non-cleared derivatives. This month I will cover the additional challenges for risk management and reporting that would arise with a pre-cessation announcement. A LIBOR pre-cessation announcement from the FCA could occur by the end of 2020. This was first discussed publicly in June […]