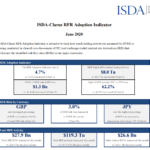

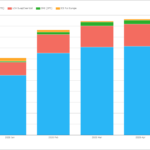

ISDA-Clarus RFR Adoption Indicator Analysis – June 2020

4.7% of derivatives risk was transacted versus an RFR in June 2020. June 2020 was a record month for the proportion of risk transacted versus SOFR in USD markets. €STR is at the beginning of adoption following the CCP discounting switch last week. JPY TONA sees a significant proportion of risk transacted in longer maturities. […]

ISDA-Clarus RFR Adoption Indicator

The ISDA-Clarus RFR Adoption Indicator was at 4.7% in June 2020. This indicator measures the risk-weighted (DV01) percentage of trading activity that takes place in RFR products. Five further sub-indicators have been developed in conjunction with ISDA, providing market participants with granular transparency into RFR activity. Check out the first publication to learn about RFR […]

Managing IBOR Transition – Fallback Spreads

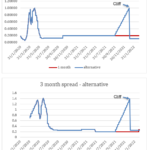

Last month I wrote about the potential for a very non-linear transition when LIBOR is discontinued. This was also covered in a recent Risk article: ‘Beware the cliff edge in Libor fallbacks’. The impending announcement on the timing of LIBOR cessation process was covered by Chris Barnes earlier this month, Also with the potential for […]

SONIA Q2 2020 Update

43% of GBP risk transacted in Q2 2020 was in SONIA. And only 24% of GBP notional was in LIBOR. Now that volatility has died down somewhat there is less short-dated trading activity. Can we consider the market standard as SONIA yet? The first Monday in March 2020 will likely be remembered for many reasons. […]

LIBOR Discontinuation has been Preannounced

LIBOR will probably see an announcement towards the end of this year that it will be discontinued. This was announced by the FCA on 22nd June. This has moved markets already because it impacts the dates to be used to calibrate the fallback spreads. This means that we have already seen the last 6 month […]

ISDA Fallback Spreads – Predicted and Alternative Scenarios

ISDA continues to make progress towards providing more certainty about the way forward for derivatives post LIBOR. This includes the calculation of the ‘fallback spread’ which is to be applied to the preferred fallback compounding methodology to minimize value transfer when the fallback is triggered. The fallback spread is calculated as the 5-year median difference […]

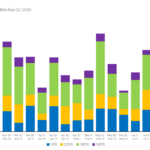

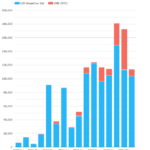

SOFR Futures and Swaps – May 2020

Open Interest in both Futures and Swaps is increasing Record volumes in recent months Volumes by CCP or SEF Basis and OIS Swap products Clarus Data Products provide insights Monthly Volumes in 2020 In CCPView we can view both volume and open interest by month. CME ETD with $5.2 trillion of Futures volume in Mar-20, […]

Cross Currency Swap conventions in an RFR world

In January 2020, the ARRC published the final recommendations for cross-currency swap conventions. It should be noted that the recommendations are primarily directed towards dealer-dealer trades and the publication points out that dealer-end user trades may require different structures. I have commented previously on potential options in AUD markets and more generally for other currencies. […]

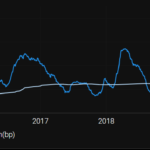

What has happened to USD LIBOR Fallback Spreads?

The fallback spread is an essential component of the LIBOR cessation plan and represents the credit and liquidity component of LIBOR relative to Risk Free Rates (RFRs). In a case where a benchmark like USD LIBOR ceases to publish, fallbacks such as compounded SOFR plus the spread are used to replace the failed benchmark. ISDA […]

Benchmarks in times of high volatility

Important current benchmarks like LIBOR, other IBORs and ICE SwapRate can have challenging characteristics during periods of high volatility. In some cases, price discovery can be difficult, which can be costly for some users and conversely rewarding for others. In this blog I will look at a few of the current benchmarks and some of […]